Cannabis Financing Options: Loans, Credit & Working Capital

Cannabis Financing Options: Loans, Credit & Working Capital

You need cash to grow your cannabis business, just like any other company. But the way you get that cash looks very different. Federal law still treats cannabis as a controlled substance, and that one fact shapes almost every financing decision you'll make.

The rules are still shifting. In April 2026, the Department of Justice moved marijuana in FDA-approved drug products and state-licensed medical marijuana from Schedule I to Schedule III. A separate DEA hearing is underway to decide whether to reschedule marijuana more broadly, with a decision expected by mid-July 2026.

None of that changes your picture today if you run a recreational cannabis business, but it signals where federal policy is headed and why more lenders are starting to pay attention to this industry.

If you’re looking for ways to fund your business, it’s important to understand what cannabis financing is, who needs it, the obstacles you're up against, and financing options worth comparing before you commit to one.

Key takeaways:

- Cannabis businesses face unique funding obstacles due to regulatory restrictions and limited access to traditional financing.

- Direct and ancillary cannabis businesses both need capital for growth, compliance, and operations.

- Vendor credit, private investors, and procurement platforms offer flexible financial solutions when bank loans are out of reach.

- Order.co gives its cannabis customers access to capital and working capital solutions without a traditional loan.

Download the free ebook: Grow Your Cannabis Business–Overcome These Three Finance Challenges

What is cannabis financing?

Cannabis financing is the process of getting business capital to cover the costs of running your cannabis-related company. Dispensaries are what most people picture when they think of a cannabis business, but if you run a cultivation operation, a medical marijuana clinic, or another related business, you need funding too.

Traditional financial institutions and lenders can provide cannabis business loans, but you're more likely to end up getting financing from private investors or venture capitalists instead due to the stigma attached to cannabis products.

The financing options typically available to you as a cannabis startup include:

- Personal loans

- Home equity lines of credit (HELOCs)

- Business loans or cannabis lines of credit

- Vendor cash advances

- Credit union loans

- Equipment financing and leases

- Investments from accredited investors

- Angel investments

- Crowdfunding

- Backing from friends and family

Some of these are harder to come by than others. Traditional loans may not be available to you at all. For private loans, you'll need to demonstrate your creditworthiness and show what sets your business apart, especially when new competitors open up in your state shortly after legalization.

Whichever form of financing you choose, you'll need to carefully examine the legal considerations, interest rates, and risks involved in running a cannabis business so you can get the working capital you need while protecting your assets.

Grow Your Cannabis Business: Overcome These Three Finance Challenges

The cannabis industry is experiencing a once-in-a-lifetime boom. Don't let poor cash flow keep you from cashing in.

What types of businesses need cannabis financing?

There are two types of businesses in the cannabis industry: direct and indirect.

- Direct cannabis businesses are those that "touch the plant," such as cultivators, dispensaries, distributors, and laboratories.

- Indirect businesses support the direct industry with services like packaging, technology, and equipment.

Direct cannabis businesses

If you're a cultivator, you grow cannabis plants and components like CBD for medicinal and recreational use. You adjust nutrient levels and control temperature and humidity to create strains with specific characteristics, all while following government regulations and product standards.

If you're a processor, you turn raw cannabis material into products like edibles, oils, concentrates, and tinctures. This involves extraction, refinement, and packaging, all under strict regulatory standards for safety and quality. Depending on your state's laws, you may have to buy finished products from processors within your own state.

If you run a laboratory, you test product samples for potency, terpenes, and contaminants. Your results help the industry meet regulatory requirements and give cultivators the information they need to make good decisions. You might also offer genetic profiling to trace a plant's origin and authenticate the product.

If you're a distributor, you connect cultivators and retailers, moving cannabis goods safely and securely while meeting compliance and taxation rules. You likely also handle inventory management, security, and product tracking.

If you run a dispensary, you're a regulated store where people buy cannabis and cannabis products for medical or recreational use. Your staff help customers find the right strain or product for their needs, whether that's therapeutic or personal use.

Indirect cannabis businesses

Indirect cannabis businesses face different financing hurdles. Still, you need financing to buy from dispensaries and other cannabis businesses, which makes these options just as important to your success.

If you run a packaging company, you provide printing, branding, and warning labels for cannabis products, along with custom designs that help products stand out. You also help protect product integrity by meeting health and safety rules, such as child-resistant or tamper-proof packaging.

If you're an equipment provider, you make and maintain the tools the industry runs on, from grow tents and trimming machines to commercial dryers, extractors, and decarboxylators. You also supply equipment like HVAC systems and water chillers and support cultivators with installation, maintenance, and repair.

If you run a technology company, you build software for inventory management, compliance tracking, and mobile operations, along with analytical tools that help growers optimize production and stay compliant with local regulations.

What are the obstacles to cannabis financing?

You face real obstacles when you try to get cannabis business financing in the US. Even as more states relax their rules on medical or recreational cannabis, the drug remains a Schedule I controlled substance at the federal level. While that may soon change, you're likely still operating in the same federal gray area the industry has been in for years if you sell recreational cannabis or hold a state license.

Federal prohibition keeps many banks and traditional lenders from accepting the risk of funding your business. It also means you can't get favorable loans from the Small Business Administration (SBA). Lenders that do take on the risk often build it into your interest rate, charging you more than they'd charge a typical company.

Two federal rules make banks especially cautious about financing cannabis-related businesses: the Anti-Money Laundering Act (AML) and the Bank Secrecy Act (BSA).

- The AML requires banks to report suspicious transactions related to money laundering and other illegal or unethical activity.

- The BSA requires banks to report all transactions over $10,000 and follow strict recordkeeping rules.

Together, these requirements make cannabis too risky for many lenders to touch. The ones that do offer financing to the industry often limit it to ancillary businesses, like general vendors, labeling and packaging companies, and point-of-sale providers built for cannabis retailers.

This gap is exactly where direct cannabis lenders and business finance companies built for the industry come in, along with vendor financing arrangements that don't require a bank at all.

Pros and cons: 8 cannabis financing options compared

Before you choose a financing option, it helps to see them side by side. Here's how the most common paths compare.

| Option | Pros | Cons | Best for | Timeline |

| Bank loans or lines of credit | Lower interest rates than alternative lenders | Hard to qualify for; most banks avoid cannabis entirely | Established businesses with strong credit and a bank willing to work with cannabis | Weeks to months |

| SBA loans | Government-backed, favorable terms | Not available to cannabis businesses under current federal rules | Not currently an option for direct cannabis businesses | N/A |

| Direct cannabis lenders | Built for the industry's risk profile and compliance needs | Higher interest rates than traditional bank loans | Businesses that need capital fast and can't get approved elsewhere | Days to weeks |

| Vendor financing | No new debt on your balance sheet; ties financing to purchases you're already making | Terms vary by vendor; not all vendors offer it | Businesses that need to fund inventory, supplies, or equipment purchases | Immediate to a few days |

| Equipment financing and leases | Preserves cash; equipment can serve as collateral | Locks you into specific equipment; may include high fees | Businesses buying cultivation, extraction, or packaging equipment | Days to weeks |

| Private investors or venture capital | Access to larger amounts of capital; investor expertise and connections | Requires giving up equity and some decision-making power | Businesses ready to scale and open to outside ownership | Months |

| Crowdfunding | No debt; builds community support | Unpredictable results; requires marketing effort | Consumer-facing brands with an engaged audience | Weeks to months |

| Procurement platforms (like Order.co) | Extended payment terms and working capital tied directly to your purchasing, without a traditional loan application | Focused on purchasing and working capital, not general-purpose cash | Businesses that need capital for supplies, equipment, and vendor purchases | Immediate to a few days once set up |

What are the requirements for obtaining cannabis financing?

Requirements vary by state, but you'll typically need to meet the following:

Strong personal credit rating: A strong credit rating is important for securing financing. For the major credit bureaus, a score of 670 or above is considered "good". A high score gives lenders confidence you'll make payments on time, though it won't guarantee your approval or a low rate.

Adequate credit history: Lenders want to see a track record of borrowing money and paying it back. They'll review your credit history, checking for recent activity and any missed payments. A strong score paired with a long history of on-time payments makes lenders more comfortable taking on the risk of working with you.

Bankruptcy-free credit history: Lenders are already cautious with cannabis funding. Any sign that you didn't repay debt in the past is a major red flag. Bankruptcy stays on your credit report for up to 10 years and can factor into a lender's decision.

Business account: You'll need a separate business bank account for cannabis lending, since it meets the increased reporting and regulatory requirements that come with cannabis financing. Set up your account under your business taxpayer identification number (TIN) along with any state filing requirements or permits.

US citizenship or resident status: You'll need US citizenship or residency to borrow money for your cannabis business. Rules around lending and permits vary by state, so it's worth consulting an attorney who knows the specifics.

Business plan: You'll need a documented business plan with projected revenue, a mission statement, a SWOT analysis, and marketing plans as part of your financing application.

Uses for cannabis financing

Like other retail or medical businesses, if you run a brick-and-mortar cannabis business, such as a dispensary or cultivation operation, you need to source real estate, supplies, inventory, technology, and services to keep running.

Your financing will typically go toward:

- Purchasing or leasing office, manufacturing, or cultivation space

- Equipment to produce, test, or refine cannabis products

- Overhead expenses such as payroll, taxes, and other operational costs

- Research and development for new products and processes

Risk and cash flow issues specific to the cannabis industry can make it hard for you to get the equipment and space you need to get off the ground.

Alternatives to traditional cannabis financing

Traditional loans aren't your only path to capital. If you have less access to bank financing, you can turn to group buying, vendor credit, or procurement platforms instead.

- Group purchasing organizations (GPOs) are third-party organizations that sell supplies to their members at a discount. They help you get the supplies you need without applying for a loan.

- Vendor financing works differently than a bank loan. Instead of borrowing cash up front, you get extended payment terms directly from your vendor or from a platform that manages vendor payments, so the money you need to buy supplies or equipment stays in your business longer. This is a distinct option from traditional lending and one that's growing as more vendors look for ways to support cannabis buyers.

- Some procurement platforms offer vendor networks and working capital access built for cannabis-focused businesses. These platforms give you price comparisons, reporting, and spend management features that help you save time and money when sourcing from vendors, all while staying competitive in your market.

For example, BrightFarms, an indoor farming operation with similarly complex, multi-location purchasing needs, used Order.co to centralize vendor management and consolidate invoicing across its sites, the same kind of setup that helps cannabis businesses manage vendor relationships and financing in one place.

Expert perspective on cannabis financing trends

The financing landscape for the cannabis industry is changing faster than it has in years. The partial move to Schedule III for FDA-approved and state-licensed medical marijuana products, combined with the DEA's ongoing review of broader rescheduling, has more traditional lenders watching the space closely, even if most still aren't ready to fund it directly. In the meantime, a new group of direct cannabis lenders and vendor financing arrangements has stepped in to fill the gap left by banks.

For cannabis businesses, that shift means more financing options than existed even a year or two ago, but also more choices to evaluate. You'll come out ahead if you treat vendor relationships and working capital access as part of your financing strategy, not just a backup plan for when a bank loan falls through.

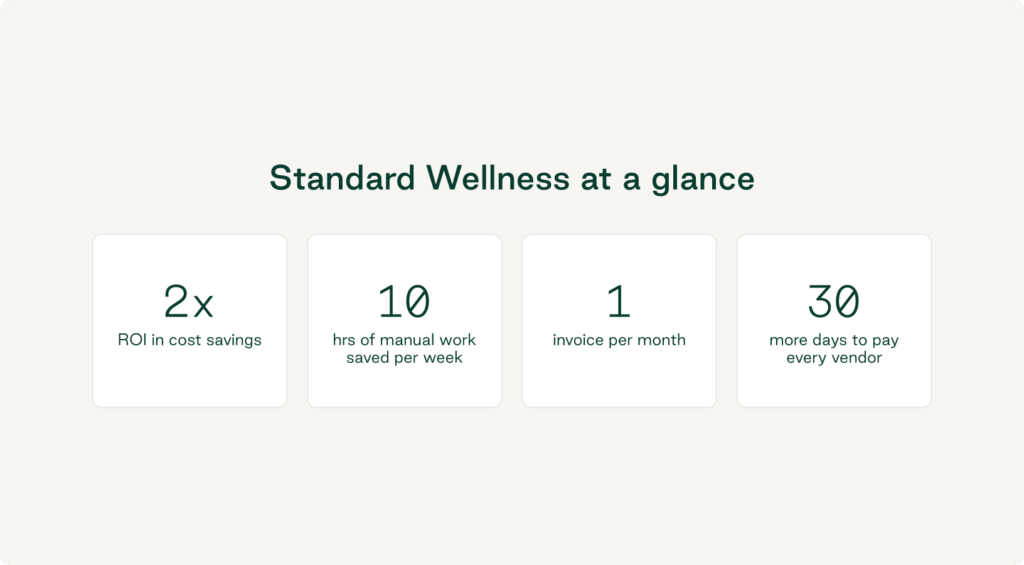

Standard Wellness, a multi-state cannabis operator, saw this play out directly. When a flower-filling machine broke down, Purchasing and Procurement Coordinator Mikey Haverman needed capital fast, and traditional financing for equipment like this had always been a "very convoluted process."

Using Order.co's Buy Now, Pay Later offering, Standard Wellness secured the funds quickly. "We were able to secure the cash in two days," Haverman said, a timeline that would have been out of reach with a traditional bank loan. Standard Wellness has also doubled their ROI in cost savings, saved 10 hours of manual work per week, and had 30 more days to pay their vendors working with Order.co.

Grow Your Cannabis Business: Overcome These Three Finance Challenges

The cannabis industry is experiencing a once-in-a-lifetime boom. Don't let poor cash flow keep you from cashing in.

"*" indicates required fields

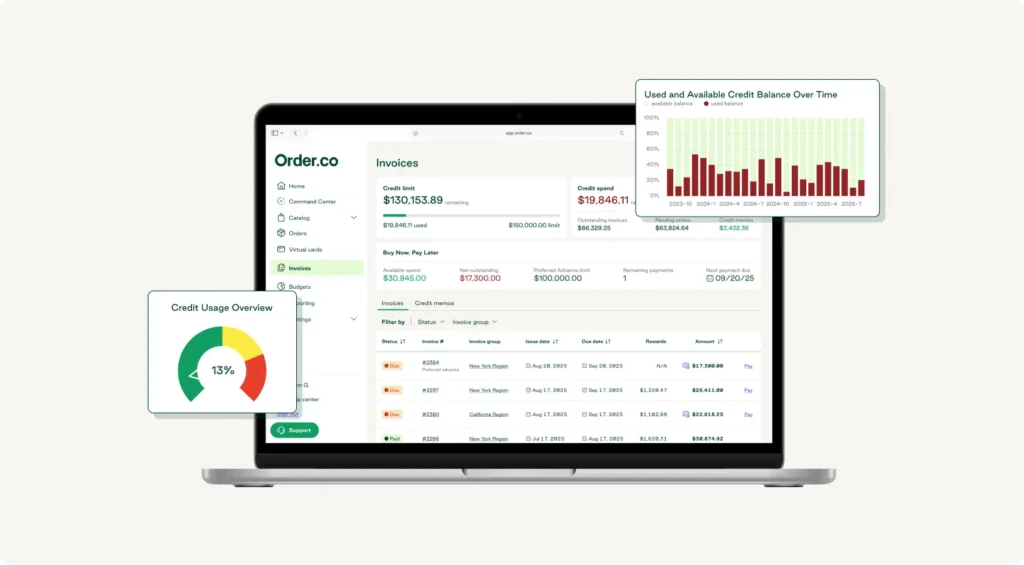

How Order.co approaches cannabis financing

Order.co takes a different approach to cannabis financing, giving you and your vendors reliable access to capital in a way that reduces risk for everyone involved. This removes many of the obstacles keeping your business from reaching its full potential.

With vendor access and working capital through Order.co, you can get up and running, source equipment, expand into new locations, and explore wider markets.

Here's how it works:

- You sign up with Order.co to buy supplies and equipment from your preferred vendors.

- Order.co provides extended net terms with a straightforward verification process.

- The platform acts as your buyer of record, removing many of the restrictions that would otherwise block you from doing business as usual.

- For larger purchases, Order.co provides up to $500,000 in working capital to fund equipment purchases and other growth activities.

- Extended terms and capital access let you get up and running quickly and start generating revenue before repayment begins.

- As revenue comes in, your cash conversion cycle shortens, so you can use financing to grow and stabilize your cash flow.

Order.co gives you the capital and vendor access you need to compete in new markets, offering an advantage as cannabis access expands into new states and territories. The platform doesn't change its rates or capital access based on the perceived risk profile of your business.

Other sources of cannabis financing

You have ways to fund your cannabis business outside of traditional financing. As legalization spreads across the US, you'll find more investment options available to fund your operations.

- Private equity: You can raise capital by selling a portion of your shares to investors. This lets you raise funds without taking on debt, giving you liquidity for operations, expansion, or research and development. In exchange, your investors get a share of future profits and decision-making power proportional to their investment.

- Debt financing (private loans): Debt financing means borrowing from private lenders, like angel investors, and paying back the principal plus interest within a set timeframe. You might choose private loans to get funding without running into regulatory roadblocks.

Both options have their use cases. For example, if you're eyeing new markets, the future value of the cannabis industry makes private equity a strong option for getting off the ground and fueling growth. If you want to keep full ownership of your business, debt financing is more appealing, since it doesn't require giving up equity. Instead, it lets you use future revenue to fund immediate needs or expansion.

Debt financing comes with its own challenges, though. You'll need enough cash flow to cover repayments, and interest rates can run higher than traditional financing. Even so, private loans offer you a real path to capital if you want to grow without diluting ownership.

Case study: Grasshopper Farms secures financing and recoups a vendor loss

Grasshopper Farms grows sun-grown cannabis flower across farms in Michigan, Colorado, and New Jersey. Running multiple farms means managing hundreds of products and vendors at once, and every one of those relationships carries financial risk if a vendor falls through.

Grasshopper Farms turned to Order.co to centralize purchasing across more than 950 products and secure $100,000 in financing, giving the team one place to manage vendors, track spend, and access capital instead of juggling separate systems for each farm.

Order.co also helped Grasshopper Farms recoup $70,000 on a separate occasion when a vendor went bankrupt. Grasshopper Farms had already paid that vendor for equipment they never received, and with Order.co’s assistance, they recouped the full amount they lost.

Founder and CEO Will Bowden sums up the impact: "We were actually able to recoup the $70k that we had paid the vendor for equipment that we never received because Order.co took care of it."

Ready to grow? Get Order.co

Beyond its advantages for your cannabis business, Order.co gives you an easy-to-use interface to discover new vendors, find the best pricing and terms, and use centralized spend data to grow your business:

- Add your preferred vendors and create curated buying catalogs to keep your spend compliant and your ordering high-quality.

- Use Order.co's financial offerings to access extended net terms and capital advances for purchases of all kinds.

- Rely on detailed reporting to stay compliant with financial regulations and show investors how efficiently you spend.

To see how Order.co can help you grow your operations, request a demo.

FAQs about cannabis financing

Turn to financing built for the industry. Procurement platforms like Order.co extend net terms and working capital without traditional bank underwriting, so you're not waiting on a lender who may never say yes. Federal restrictions keep most banks and SBA lenders away from plant-touching businesses, which drives up rates. Order.co's model gives you flexibility to cover costs and manage the added pressure of 280E, so financing barriers don't have to slow your growth.

Tight cash flow management is what keeps you steady when traditional financing isn't an option. Cannabis runs mostly on cash, since many banks still won't hold cannabis deposits, and margins are squeezed further by the 280E tax code. Demand can also shift fast with new regulations or licensing changes. Without a credit line to fall back on, a cash gap can stall payroll or inventory overnight. Managing cash flow well lets you absorb a slow month and keep investing in growth.

Order.co automates your purchasing and payments while giving you working capital, so you can scale operations without adding headcount. Purchasing automation cuts the manual work of chasing invoices and reconciling vendor payments, and consolidated spend gives you better pricing leverage with vendors. AI recommendations surface better-priced vendors and flag pricing drift before it costs you money. Built-in working capital means you're not waiting on a bank to fund growth, and consolidated visibility helps you stay compliant as regulations shift.

If your cannabis business doesn't touch the plant directly, like packaging vendors, testing labs, or software providers, you face fewer legal restrictions than plant-touching operators. That lower regulatory exposure makes you look like a standard small business to a lender. You can access conventional loans and lines of credit at lower rates, options that most plant-touching cannabis companies can't get. Staying one step removed from the plant simplifies financing and cuts the higher rates directly-touching operators often pay.

Cannabis vendor financing means a vendor, or a platform that manages vendor payments, gives you extended payment terms instead of requiring payment up front. This lets you get the supplies or equipment you need right away while paying for them over time, without applying for a traditional loan.

Get started

Schedule a demo to see how Order.co can simplify buying for your business.

"*" indicates required fields