Credit Cards for Employees: Best Options in 2026

Credit Cards for Employees: Best Options in 2026

For many employees, expense management is a recurring source of frustration. They pay out of pocket, track receipts, and wait weeks to get reimbursed. Finance teams carry the other half of the problem, spending hours chasing receipts and reconciling expenses instead of doing more strategic work.

Credit cards for employees solve both sides of the problem. They give your team immediate access to company funds, so people stop reaching for personal cards or skipping processes to get what they need. And they give finance real-time visibility, faster reconciliation, and lower fraud risk as the business grows.

Choosing the right employee card setup requires evaluating how your team buys, comparing top options on the market, and establishing clear controls to issue cards safely.

Quick answer:

- Employee credit cards are company-issued cards with preset limits and built-in controls, so the business holds liability instead of the individual.

- For finance, the payoff is real-time spend visibility, fewer manual reconciliation hours, and lower fraud risk.

- For employees, company cards remove the pay-out-of-pocket-and-wait cycle, so fewer people resort to personal cards or workarounds.

- The right option depends on your priorities. Traditional cards compete on rewards and credit terms, while corporate cards and procurement platforms compete on control, automation, and visibility.

- Order.co brings purchasing, vendor-locked virtual cards, automated payments, and line-item GL coding into one platform. Buyers shop from pre-approved catalogs or virtual cards, and the software automatically codes every line item, giving finance real-time visibility into spending as it happens.

Download the free ebook: Choose the Right Procurement Technology With This Decision Matrix

What are employee credit cards, and how do they work?

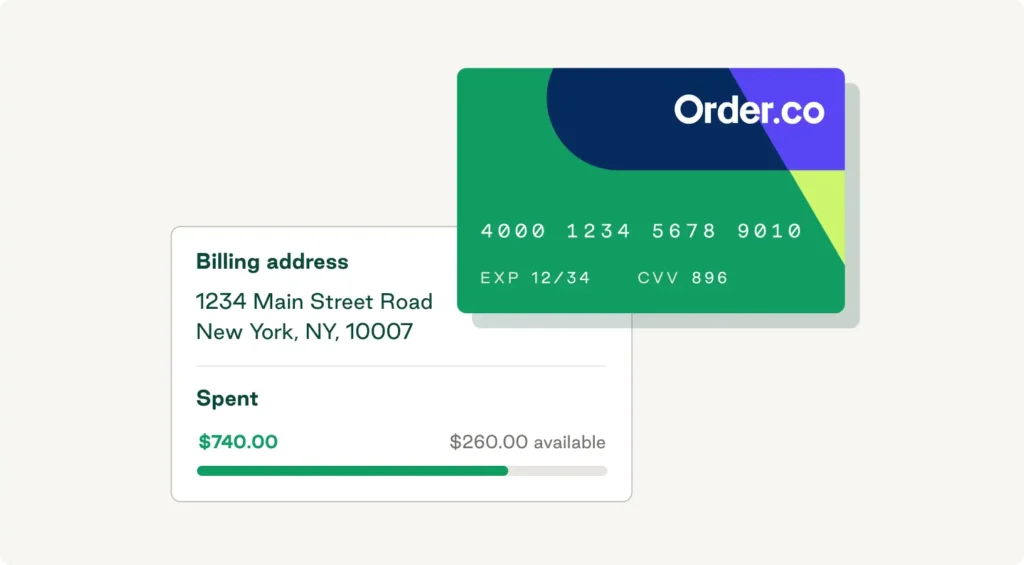

Employee credit cards, including corporate cards and purchasing cards or P-cards, are company-issued cards teams use for business expenses like travel, departmental purchases, and recurring software subscriptions. The company issues them and holds the liability, protecting the individual employee's personal credit.

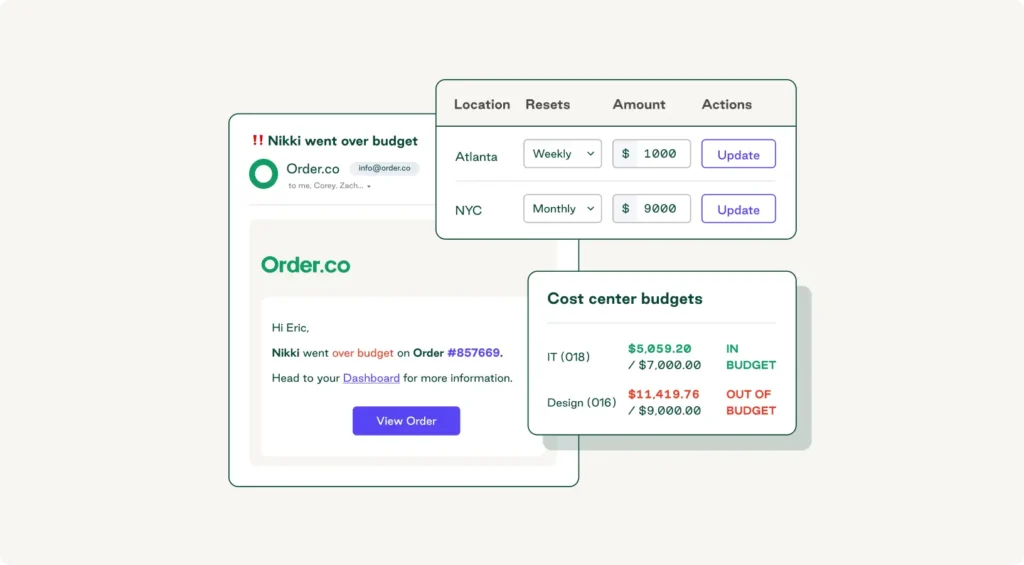

A finance or card administrator sets each card up with a preset spending limit and, in many cases, vendor or merchant-category restrictions, so purchases comply with internal policy without requiring separate approvals for each transaction. When you connect a card with your accounting system, every transaction gets categorized and coded automatically, which speeds up reconciliation and gives finance ongoing oversight of company spend.

According to a 2024 Visa survey, 79% of businesses already use credit cards for payments, so for most teams, the question is how to run the program well rather than whether to use cards at all.

Choose the Right Procurement Technology With This Decision Matrix

Find 15 must-ask questions to narrow down your software search and make your research process MUCH easier.

How are employee credit cards different from other cards?

Employee credit cards are user- or department-specific, with pre-configured controls that enforce your spending policies. Understanding how they compare to other payment options helps you choose the right fit.

| Card feature | Employee credit cards | Personal credit cards | Corporate debit cards |

| Liability | The company assumes all responsibility | The individual assumes all responsibility | The company assumes all responsibility |

| Credit impact | No impact on the cardholder's credit score, may build business credit | Directly affects the cardholder's credit report and builds personal credit | No credit implications, doesn’t build credit |

| Controls | Customizable limits and restrictions that enforce internal policies | Limited options, based on personal creditworthiness | Limits determined by available account balance |

| Rewards | Accrue to the company, vary by program | Earned by and belong to the individual | Typically none |

| Reimbursement | Not required, the company pays directly | Employees must request reimbursement | Not required |

What are the benefits of issuing credit cards for employees?

Finance teams issue employee cards to make team spending more efficient and visible. A good program eliminates out-of-pocket reimbursements, provides real-time data on where money goes, and reduces fraud risk as you add locations and headcount.

Some cards also offer perks like cash back or travel points, which can offset program costs, though for most finance teams, the bigger returns are the time saved and the control gained.

Enhanced expense tracking

Manual expense reporting is time-consuming and error-prone, and small mistakes create reporting gaps that slow down your close. Employee credit cards give you real-time visibility into card activity, so you can catch budget overruns early and manage spend as it happens. Each transaction is classified automatically and sent to your accounting system, which reduces errors and speeds up reconciliation.

Reduced risk of fraud and misuse

Any payment method carries some risk of fraud or accidental misuse, but employee cards reduce that risk with built-in safeguards that block unauthorized purchases before they occur.

Vendor-locked virtual cards tie each card to a single vendor, so even if that vendor has a data breach, only one card is exposed. Real-time alerts flag suspicious activity instantly, which helps you stop fraud before funds leave your account.

To examine these aspects in more detail, take a closer look at whether virtual cards are safe.

Tax implications of employee credit cards

Employee cards simplify tax time if you keep clean records. Because every purchase is logged, you have a clear trail of deductible business expenses without needing to dig through reimbursement requests.

Keep the receipt, the business purpose, and the cardholder attached to each transaction so your records hold up if you're ever audited. To ensure what you buy actually qualifies as deductible, look to the IRS guidance on business expenses. Keeping business purchases and personal spending on separate cards also makes your reporting cleaner and lowers audit risk.

Best practices for issuing company credit cards to employees

Card programs work best with a bit of structure. A clear policy, role-based controls, and a regular review keep spending compliant as you scale.

Create a corporate card policy

Your card policy should spell out who qualifies as an authorized user, what they can buy, and what happens if the rules are broken. Cover:

- Eligible cardholders by role or business need

- Approved and prohibited expense categories

- Spending limits by role or department

- Receipt and documentation requirements

- Consequences for misuse

Bring in stakeholders from the teams that will actually use the cards so the policy fits how they work.

Set spend controls

Spend controls are your best defense against unauthorized spending. Useful controls include transaction limits, daily or monthly caps, merchant-category restrictions, vendor locks, geographic limits, and time-based rules.

Build these into your policy and have employees acknowledge them before they get a card. With a platform like Order.co, you can instantly generate and issue virtual cards with the right limits already attached.

Audit spend regularly

Regular audits catch what your automated controls miss. Set a steady rhythm. Review transactions for red flags like duplicate charges or unusual spikes, check each department's spend against budget, and run a deeper annual review of company policy and compliance. Share what you find with cardholders and team leads so you can fix issues early and reinforce good habits.

Best business credit cards for employees and team spending

Different cards fit different needs. Traditional business credit cards compete on rewards and credit terms, while corporate card and procurement platforms compete on control, automation, and visibility.

The options below cover both, so you can match your choice to how your team buys. For a wider look at card types, compare virtual cards vs. purchase cards.

Employee credit card comparison table

| Option | Type | Best for | Standout strength |

| Order.co | Procurement and spend platform (virtual cards) | Procurement and spend control | Control built in before money is spent |

| Ramp | Corporate card and expense software | Automated expense management | Hands-off receipt and expense automation |

| Brex | Corporate card | Startups and high-growth teams | No personal guarantee, fast issuance |

| Chase Ink Business Unlimited | Traditional business credit card | Simple cash back | Flat 1.5% cash back, no annual fee |

| Amex Business Gold | Traditional business credit card | Rewards optimization | High points on top spend categories |

Choose the Right Procurement Technology With This Decision Matrix

Find 15 must-ask questions to narrow down your software search and make your research process MUCH easier.

"*" indicates required fields

1. Order.co: Best for procurement and spend control

Order.co is an AI-powered procurement and finance automation management platform rather than a traditional card issuer. Its B2B virtual cards sit inside a system that also handles purchasing, approvals, payments, and reconciliation as a full procure-to-pay platform, so card spend connects back to the rest of your buying.

Control starts at the catalog level, where only pre-approved products and vendors are visible to buyers, so the compliant choice is also the easy one. Order.co is virtual-only and does not issue physical cards.

2. Ramp: Best for automated expense management

Ramp pairs corporate cards with expense automation. It's built to cut manual expense work and surface savings through real-time tracking of employee spending.

Key features:

- Physical and virtual corporate cards

- 1.5% cash back on purchases

- Automated receipt capture and categorization

- Bill pay for vendor invoices

- Real-time spend tracking and reporting

Best for: Teams that want hands-off expense management

Considerations: Ramp codes spend at the transaction level rather than by line item, so the most granular purchasing detail is limited.

3. Brex: Best for startups and high-growth teams

Brex offers corporate cards built for startups and high-growth companies, with limits based on your cash balance rather than personal credit.

Key features:

- Corporate cards with no personal guarantee

- Credit limits based on company cash, not personal credit

- Built-in expense management and accounting integrations

- Rewards on common business spend categories

- Fast digital card issuance

Best for: Venture-backed startups and fast-scaling teams

Considerations: The model favors companies with healthy cash balances or funding, so it may not suit every business stage.

4. Chase Ink Business Unlimited: Best traditional cash-back card

Chase Ink Business Unlimited is a traditional business credit card with flat-rate rewards and no annual fee.

Key features:

- 1.5% cash back on every purchase

- No annual fee

- Free employee cards

- Intro APR offer on purchases

- Standard purchase and fraud protections

Best for: Businesses that want simple cash back without tracking categories

Considerations: Approval depends on credit, and spend controls are lighter than a dedicated spend platform.

5. American Express Business Gold Card: Best for rewards optimization

The American Express Business Gold Card is built to maximize rewards on your biggest spend categories.

Key features:

- Elevated points on your top eligible spend categories each month

- Flexible Membership Rewards points

- Employee cards with assignable limits

- Travel and purchase protections

- Pay-over-time flexibility on eligible charges

Best for: Companies optimizing rewards on high, concentrated spend

Considerations: It carries an annual fee, and the rewards program depends on hitting category thresholds. Budget-conscious teams like nonprofits may prefer options in our guide to credit cards for nonprofits.

To compare more options, see our roundup of cash-back business credit cards, or if credit is a hurdle, business credit cards for fair credit.

How do you know which card is right for you?

Start with your priorities, then match them to the options above:

- If rewards are the goal and you have strong credit, a traditional card like Chase Ink Business Unlimited or Amex Business Gold fits.

- If you want hands-off expense tracking, Ramp is a strong option.

- If you're early-stage without an established credit history, Brex's cash-based model is worth a look.

- If your priority is control and efficiency across purchasing and payments, a procurement platform like Order.co fits best.

Weigh three things as you decide: your company size and financial position, how much policy enforcement and reporting you need, and the total cost of ownership beyond the headline rewards rate.

Choose the right credit cards for employees and keep control of spend

The right choice comes down to a few main considerations: who holds liability, how much spend control you need, how well a card syncs with your accounting system, and whether rewards matter more than automation. Traditional cards win on rewards. Procurement and spend platforms win on control, visibility, and speed.

Order.co goes beyond card-based expense tracking. It brings purchasing, vendor-locked virtual cards, automated payments, and line-item GL coding into one platform, so your team buys from pre-approved catalogs and finance sees and codes every purchase as it happens. That delivers immediate visibility and faster reconciliation, without the pay-out-of-pocket-and-wait cycle.

Book a demo to see how Order.co can replace receipt-chasing and manual coding with real-time spend control.

FAQs about credit cards for employees

With most employee and corporate credit cards, the company holds liability, not the individual cardholder. That means the business is responsible for charges, including misuse. This is why spend controls and a clear card policy matter, since they limit exposure by capping amounts, restricting merchants, and defining consequences for breaking the rules. Some traditional business cards require a personal guarantee from the owner, which shifts some liability to that individual.

In most cases, no. Employee and corporate credit cards are tied to the business, so everyday use does not affect an employee's personal credit score. The company assumes liability, and the account reports to business credit rather than personal credit. The exception is when a business card requires a personal guarantee from the owner. In that situation, missed payments or default can affect the guarantor's personal credit.

Cash back and points earned on business credit cards are generally treated as a rebate on spending rather than taxable income, so they usually are not taxed when earned. They can affect your taxes indirectly, because rewards used to reduce a business expense lower the deductible amount of that expense. Tax rules vary by situation, so check with a tax professional or the IRS to confirm how rewards apply to your business.

Get started

Schedule a demo to see how Order.co can simplify buying for your business

"*" indicates required fields