How to Choose the Best Virtual Card for Your Business in 2026

How to Choose the Best Virtual Card for Your Business in 2026

Payment fraud, slow reconciliation, and limited visibility into vendor spend stack up on AP teams every month. For multi-location businesses, traditional corporate credit cards compound these issues: shared numbers, missing receipts, manual GL coding, and no real way to stop overspend before it happens.

Virtual cards work differently. Each card carries a unique number tied to a specific vendor, user, budget, or timeframe, so compromised numbers stay contained, controls travel with the card, and finance sees spend as it moves.

But not all virtual card programs work the same way. The right choice depends on how your team actually buys, how many vendors you manage, and how much manual work lands on finance after every transaction. Virtual cards that connect to your purchasing and AP processes help contain fraud, keep approvals on-policy, pre-code spend, and give finance real-time visibility into every dollar before month-end.

Key takeaways: Best virtual cards

- Virtual cards reduce fraud exposure, simplify vendor payments, and give finance better visibility into spend—but how well they fit your team's buying process varies significantly across providers.

- The baseline is unique card numbers, per-card limits, and real-time alerts. The programs that go further connect cards to approval workflows, automate reconciliation, and actively surface savings.

- The right program depends on how your team buys, how many vendors you manage, and how much manual work currently lands on finance after every transaction.

- Order.co's virtual cards tie each card to a single vendor and budget, route spend through automated approval workflows, and give finance real-time visibility into spend.

Download the free ebook: The Procurement Strategy Playbook for Modern Businesses

Why does choosing the right virtual card matter for your business?

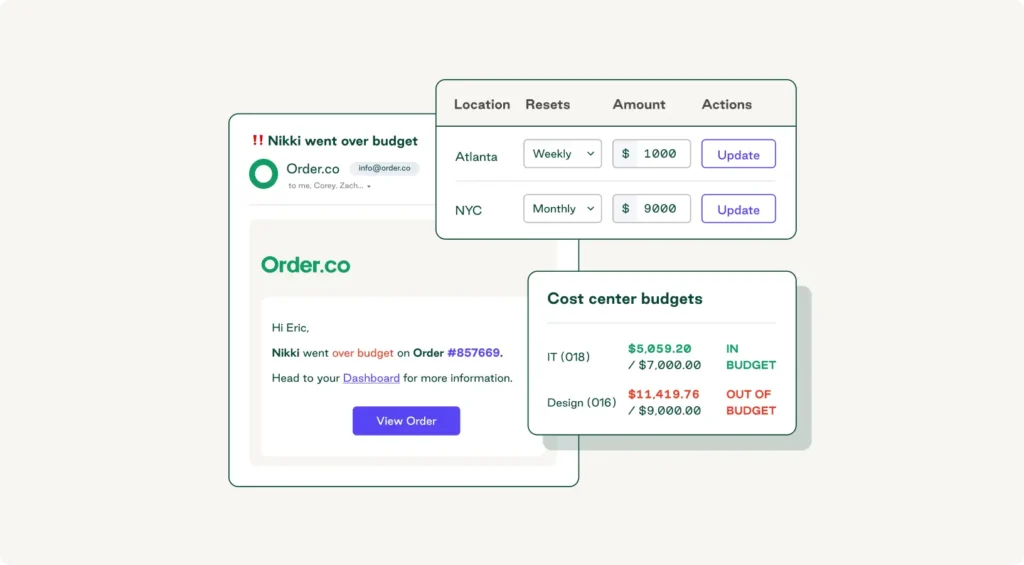

According to the 2026 AFP Payments Fraud and Control Survey, 76% of US organizations experienced attempted or actual payments fraud in the past year. Business credit card programs sit in the same threat environment, and a single compromised card number can disrupt operations for weeks.

For multi-location operators, the damage compounds at scale. A 25-property hospitality group may have 60+ active corporate cards across its operations teams. One team member's stolen card information triggers a freeze, a reissue, a scramble to find the affected subscriptions, and a stack of declined payments.

Virtual cards collapse that risk in the following ways:

- Each card is unique, so freezing one does not affect the others.

- Each card is restricted to a single vendor, user, or use case.

- Each carries its own limits and expiration, containing exposure before fraud happens.

Fraud containment is only part of the story. A recent J.P. Morgan analysis of B2B payment trends found that virtual cards have become a strategic lever for modernizing payment workflows and unlocking working capital, a shift driven by the efficiency gap between how payments work today and how AP teams actually operate.

The right virtual card program closes that gap by integrating directly with your procurement and AP workflow: transactions arrive in your ERP pre-coded, approval routing matches how your team actually approves spend, and finance sees every dollar of vendor spend in real time rather than at month-end.

The Procurement Strategy Playbook for Modern Businesses

Want to know more about strategic buying? Read our Procurement Strategy Playbook for even more valuable insights.

What are the best virtual cards to consider in 2026?

The category spans three shapes: corporate cards with virtual credit card functionality, AP automation platforms with embedded cards, and procurement platforms with cards built in. The five card options below cover the most common comparisons.

The information below is accurate as of May 2026. Verify pricing and features with each card provider before deciding.

Best virtual cards at a glance

| Provider | Pricing model | Card limits | Standout feature | Best for |

| Order.co | Quote-based; no per-card fees | Unlimited cards; per-card, per-vendor, and per-budget limits | Vendor-locked cards with line-level GL coding inside a full purchasing and AP platform | Multi-location operators managing high-volume vendor spend |

| Ramp | Free base tier; paid tiers for advanced features | Unlimited cards; per-card and business limits | AI-driven savings insights and reimbursement automation | Operators with heavy T&E, SaaS, and reimbursement spend |

| Brex | Free base tier; paid plans for premium features | Underwritten on cash balance and revenue, not personal credit | Category-based rewards and built-in banking | Funded startups and high-growth tech companies |

| BILL Spend & Expense | Free for the card program; part of BILL's integrated platform | Per-user and per-budget limits | End-to-end AP automation paired with cards | Finance teams that want one vendor for cards and bill pay |

| Airbase by Paylocity | Quote-based; tiered by company size | Per-card, per-budget, and per-vendor limits | Multi-currency support and pre-approval workflows | Companies with international vendors or strict approval cultures |

1. Order.co

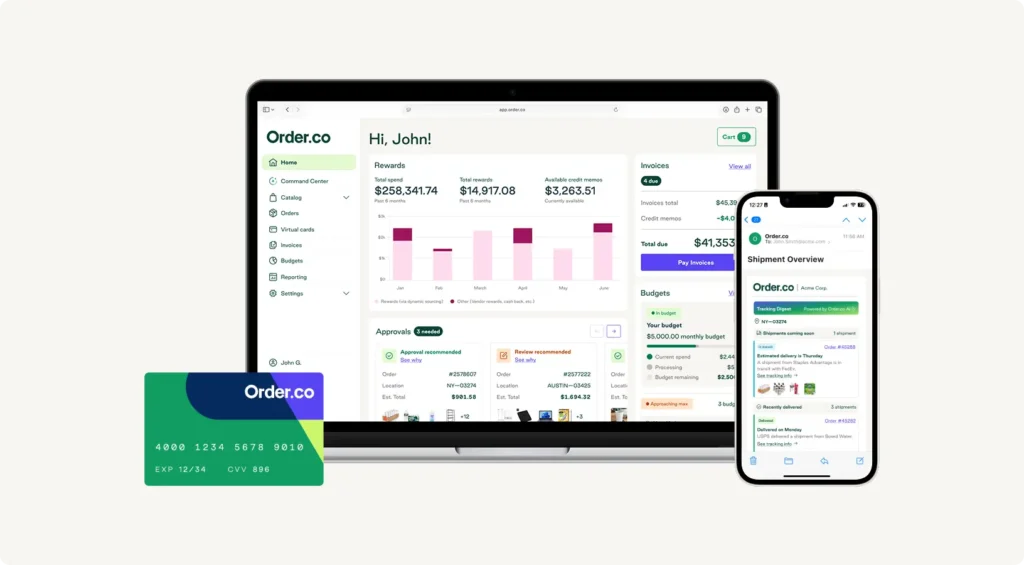

Order.co is an AI procurement and finance automation platform built for teams managing high volumes of vendor spend across multiple locations. It provides unlimited virtual card issuance with no per-card fees and granular spending rules by vendor, user, and budget.

Key features and benefits:

- Vendor-locked cards tied to a single vendor, user, and budget

- Variable cash back on card spend, plus an average of 5% hard-dollar savings through AI sourcing on purchases made through the platform

- True net 30 on every purchase, with up to 37 days to pay

- Line-item GL coding on every transaction at the moment of purchase

Best for: Multi-location operators whose largest spend is goods and services across many vendors, and who want procurement, AP, and card transactions running in a single workflow.

Considerations: Order.co's vendor card savings vary, making returns less predictable than cards with flat-rate cash back.

2. Ramp

Ramp pairs virtual cards with AI-powered spend management to automatically surface savings opportunities. Its strength shows up in T&E, SaaS, and reimbursements, where the mobile experience and receipt-matching are central to the workflow.

Key features and benefits:

- Spend analysis that flags duplicate or underused subscriptions

- Automated expense reimbursements synced to accounting software

- Per-transaction cash back on business purchases

- Built-in receipt matching that removes manual expense reports

- Real-time spend notifications through the mobile app

Best for: Finance teams running heavy T&E, SaaS, and reimbursement-driven spend, where surfacing subscription waste and automating expense reports is the primary win.

Considerations: Ramp's procurement-side workflow is lighter than dedicated procurement platforms; purchase requests and PO management aren't core. Operators managing high-volume goods purchasing across many vendors typically pair Ramp with a procurement tool.

3. Brex

Brex was acquired by Capital One in April 2026 and now operates as part of Capital One's business banking division. It targets funded startups and high-growth companies, underwriting credit limits on company financials rather than personal credit, and supports local-currency card issuance in 50+ countries.

Key features and benefits:

- High credit limits underwritten on cash balance and revenue, with no personal guarantees

- Category-based rewards: 7x on rideshare, 4x on Brex Travel bookings, 3x on dining, 2x on software, 1x on everything else

- Integrated expense management with automated categorization and receipt matching

- Travel booking with corporate rate negotiation through Brex Travel

- No foreign transaction fees across 50+ supported countries

Best for: Funded startups and high-growth tech companies with significant T&E, software, and travel spend, where category-based rewards translate to meaningful points value.

Considerations: Brex's underwriting model favors VC-backed companies with cash on the balance sheet; bootstrapped businesses or operators outside the funded-tech profile may find limits restrictive.

4. BILL Spend & Expense

BILL Spend & Expense (formerly Divvy) is BILL's corporate card and expense management product, offered free of subscription or per-user fees. Finance teams use it standalone for cards, budgets, and reimbursements, or pair it with BILL AP to extend the workflow into invoice ingestion and bill payment.

Key features and benefits:

- Virtual and physical cards with customizable spending rules, budgets, and approval policies

- Real-time budget tracking with transaction-level visibility and automatic receipt matching

- Reimbursements managed alongside card spend in a single platform

- Native integrations with QuickBooks Online, NetSuite, Sage Intacct, and Xero

- Optional pairing with BILL AP for invoice ingestion, approvals, and bill payments

Best for: Finance teams already running BILL for accounts payable, or smaller teams that want a free card program with budget controls built in.

Considerations: BILL Spend & Expense only covers cards and expenses. Teams needing PO management, vendor catalogs, or upstream purchasing controls typically pair it with a dedicated procurement platform.

5. Airbase by Paylocity

Airbase combines virtual cards, bill payments, expense reimbursements, and a procurement intake module in one platform. The product integrates with Paylocity's broader HR and payroll suite for companies that want HR and finance spend in one place.

Key features and benefits:

- Virtual and physical cards with pre-approval workflows, where each card is requested through an expense intake before issuance

- Multi-currency card issuance in USD, GBP, and EUR with local-currency compliance

- Bill payments and expense reimbursements managed alongside card spend

- Guided Procurement intake module for routing purchase requests through approvals

- Native integration with NetSuite, QuickBooks, Sage Intacct, and Xero

Best for: Companies that want pre-approval baked into card issuance, or teams already running Paylocity for payroll and HR who want spend management on the same platform.

Considerations: Airbase's procurement intake handles approvals and routing well, but lacks the catalog management, vendor sourcing, and automated fulfillment of dedicated procurement platforms. Multi-currency support is currently limited to USD, GBP, and EUR, so teams operating in other regions may need a separate solution.

What key features do the best virtual cards have?

Virtual cards vary in capabilities that determine how much manual work they create for finance after the swipe. Here’s what to consider:

- Granular spend controls. Per-card spending limits, merchant category restrictions, vendor whitelisting, single-use vs. recurring designation, and expiration dates. These features help contain exposure before fraud or overspend happens, rather than catching it during month-end review.

- Real-time monitoring and alerts. Transaction notifications, live spending dashboards, and configurable alerts that fire before a card hits its limit. Catching irregular or unauthorized spend in real time means finance can freeze a card mid-fraud, intervene before a budget overruns, or stop a duplicate subscription from billing again, before it hits the books.

- Line-item GL coding at the moment of purchase. Each transaction is tagged to the correct chart-of-accounts line as it's authorized, not categorized after the fact. The distinction matters since post-hoc categorization still requires AP review—pre-coded transactions don't.

- Native ERP integration. Direct connections to the accounting and ERP systems finance already uses (QuickBooks Online, NetSuite, Sage Intacct, Xero, Workday) that post-code transactions without manual export, upload, or reconciliation, freeing AP from line-by-line statement matching every month.

The Procurement Strategy Playbook for Modern Businesses

Learn the key pillars of a strong strategy, valuable procurement metrics to track, and initiatives you can start implementing today.

"*" indicates required fields

How to choose the best virtual card for your business

When choosing the best virtual card for your business, start with the pain you're solving for, whether that's fraud exposure, slow reconciliation, limited visibility, or overspend you can't catch in time, then run the field through four filters:

Workflow scope

Ask whether the card is the product or one piece of a larger workflow. Card-centric platforms are enough when card spend is contained (T&E, SaaS, occasional vendor payments). If most of your spend runs through POs, invoices, or vendor catalogs, cards that live inside a procurement or AP platform ensure your team doesn’t have to reconcile between a card, invoice, and ERP tool.

Cost-savings

Look for a card program that actively reduces spend, not just tracks it. The strongest programs flag duplicate subscriptions before they bill again and identify contracts due for renegotiation. For high-volume operations, those capabilities deliver hard-dollar savings that exceed the cost of the program itself.

Control depth

Per-card limits and merchant restrictions are baseline. Multi-location operators need approval routing by amount, location, and cost center, plus the ability to issue different cards for different use cases (subscriptions, marketing, one-off vendor payments), each with their own controls.

Total cost

If you need dozens or hundreds of active cards, per-card and per-transaction fees compound fast. Unlimited issuance can be the difference between a workable program and one that prices itself out. Factor in FX charges where relevant and the labor cost of manual reconciliation, since faster close and reduced fraud usually outweigh the sticker price.

Get started with Order.co virtual cards

For teams managing high-volume vendor spend across many locations, the right virtual card fits how your team already buys, adding control and visibility upstream and reducing manual reconciliation work after the fact.

With Order.co, fraud stays contained to a single vendor card, every transaction is already reconciled before it hits AP, and finance sees every dollar of vendor spend in real time. For purchases made within the procurement and finance automation platform, approval routing keeps purchases on-policy from the start and AI sourcing surfaces lower-priced vendors for an average 5% in hard-dollar savings.

Schedule a demo to see how Order.co virtual cards fit into your purchasing process.

FAQs about virtual cards

A virtual card is a unique 16-digit card number generated for a specific vendor, transaction, user, or time window, with its own CVV, expiration date, and spending controls. It works wherever credit cards are accepted online or via digital wallets, but because the virtual card number is segmented from the rest of your card program, compromised card details at one merchant won't expose any others. Finance teams use virtual cards to add a layer of security, enforce per-vendor limits, and keep vendor spend visible and contained from the moment of purchase.

The baseline includes unique card numbers per vendor, instant freeze and cancellation, merchant category restrictions, per-card limits, and real-time monitoring with configurable alerts. Tokenization for digital payments, CVV controls, and audit trails round out a strong program. For multi-vendor procurement, vendor-locked cards and line-item GL coding offer the best protection against both external fraud and unauthorized internal spend.

Yes. You can issue a dedicated virtual card for each recurring vendor with a preset limit matching the expected charge, giving you clear visibility into subscription spend, automatic flagging when charges exceed expected amounts, and the option to instantly cancel a vendor by closing the card. Each card maps to a single GL line, which keeps reconciliation clean.

Most providers follow a similar process: create an account, complete business verification using the legal entity name, tax ID (EIN), business address, and incorporation documents, then go through an underwriting step. Many use alternative underwriting that looks at bank account balance and monthly revenue alongside or in place of credit scores, which speeds approval. With Order.co, established businesses typically complete onboarding and receive cards within a few business days, and unlimited cards can be issued thereafter with no per-card fee.

Get started

Schedule a demo to see how Order.co can simplify buying for your business.

"*" indicates required fields