What Are the Best Business Credit Cards for Fair Credit? (2026)

What Are the Best Business Credit Cards for Fair Credit? (2026)

A fair credit rating may limit your options when applying for a business credit card, but it doesn't eliminate them. Plenty of card programs are built for fair-credit applicants, and a growing set of alternatives, including corporate and virtual cards, can extend your purchasing power without leaning on your personal credit score. Whether you're rebuilding credit, have steady revenue but need a higher limit, or simply want to keep spending in check, the right business credit card for fair credit depends on your goals.

Selecting a card is only one aspect of protecting your credit profile. Used alongside a fair-credit card, the right procurement platform pays vendors on terms that ease cash flow pressure, surfaces spend patterns before they become missed-payment problems, and routes purchases through approvals built into how your team already buys, so high utilization and late charges have fewer chances to develop.

Key takeaways: Business credit cards for fair credit

- Fair credit (FICO 580–669) limits but doesn't eliminate your business card options, with 640+ generally treated as the practical threshold for approval.

- Secured and unsecured cards both work for fair-credit businesses, with secured cards better suited to rebuilding credit and unsecured cards offering higher limits and rewards at the upper end of the range.

- No-credit-check corporate cards underwrite business cash flow instead of personal credit, making them an option for established businesses, though they typically don't report to bureaus.

- Your goal determines the right card. Rebuilding credit, capturing rewards on existing spend, or pairing the card with a system that fits how your team buys all point to different products.

- Order.co complements your card strategy: vendor-locked virtual cards keep each purchase tied to one approved vendor, AI sourcing surfaces 5% in average product savings on what you already buy, and up to 37 days to pay gives you more working capital than standard Net 30 terms.

Download the free ebook: Choose the Right Procurement Technology With This Decision Matrix

What counts as "fair credit"?

Fair credit covers FICO scores from 580 to 669, according to Experian's published score ranges. Good credit begins at 670. This range matters because most business card issuers use it to decide your approval odds, credit limits, interest rates, and whether a personal guarantee is required.

Fair credit shows some financial reliability, but you'll see higher APRs, lower limits, and stricter terms than cards built for stronger profiles. Most issuers treat the upper end of fair credit (around 640+) as the practical threshold for approval.

What fair credit means for business card approvals

Three things shift when you apply for a business card with fair credit:

- Personal guarantees. Most fair-credit business cards require a personal guarantee, meaning you're personally liable if the business defaults. Some no-credit-check corporate cards skip this, but they typically require an LLC or corporation structure and underwrite the business's cash flow instead.

- Credit limits. Fair-credit cards generally start in the $1,000–$5,000 range, often significantly lower than what excellent-credit applicants see. Limits typically increase after 6–12 months of on-time payments.

- Interest rates. APRs for fair-credit cards typically run higher than prime-borrower rates, which makes carrying a balance more expensive and increases the cost of any missed payment.

If you're at the upper end of fair credit, those terms are still manageable. If you're closer to the lower end, secured cards or no-credit-check corporate cards may be a better entry point.

Choose the Right Procurement Technology With This Decision Matrix

Find 15 must-ask questions to narrow down your software search and make your research process MUCH easier.

Secured vs. unsecured business credit cards

Fair-credit business owners generally choose between two card types:

- Secured cards require an upfront security deposit that usually equals your credit limit. They're easier to qualify for, which makes them well-suited to rebuilding credit or establishing a business credit history from scratch. The cost is liquidity. You tie up cash in the deposit, and your limit is capped by what you can put down.

- Unsecured cards require no deposit, often carry higher limits, and typically include a rewards program. Within the fair-credit range, approval typically requires the upper end (the 640+ threshold most issuers treat as the practical cutoff), and APRs and fees can run higher than on secured alternatives.

Neither path is universally better. The right choice depends on your available cash flow, how aggressively you want to build credit, and how comfortable you are with the risk profile of each. If you're focused on rebuilding credit, start with a secured card and move to an unsecured one once your score improves.

Best business credit card options for fair credit (2026 comparison)

The cards below cover unsecured, secured, and no-personal-credit-check options that accept fair-credit applicants. Verify rates and terms with the issuer before applying.

Fair credit business cards at a glance

| Card | Min. FICO | Annual Fee | Rewards/Savings | Secured | Approval Odds |

| Order.co virtual cards | No personal FICO check | $0 | Variable cash back on spend; up to 5% savings on platform purchases with AI sourcing enabled | No | Based on company cash flow |

| Capital One Spark 1% Classic | ~580 | $0 | 1% cash back; 5% on hotels/rental cars via Capital One Travel | No | Fair |

| Capital on Tap Business Credit Card | ~580–670 | $0 | 1.5% cash back on all spend | No | Fair to Good |

| Bank of America Business Advantage Unlimited Cash Rewards Secured | No minimum (deposit-based) | $0 | 1.5% cash back on every purchase | Yes ($1,000 min. deposit) | High (secured) |

| FNBO Business Edition Secured Mastercard | No minimum (deposit-based) | $39 | Mastercard Easy Savings rebates | Yes ($2,000–$10,000 deposit) | High (secured) |

| Ramp Corporate Card | No personal credit check | $0 | 1.5% cash back; partner discounts | No (requires LLC/Corp) | Based on company cash flow |

| BILL Divvy Card | No personal credit check | $0 | Tiered rewards on dining, travel, recurring software | No (requires LLC/Corp) | Based on company cash flow |

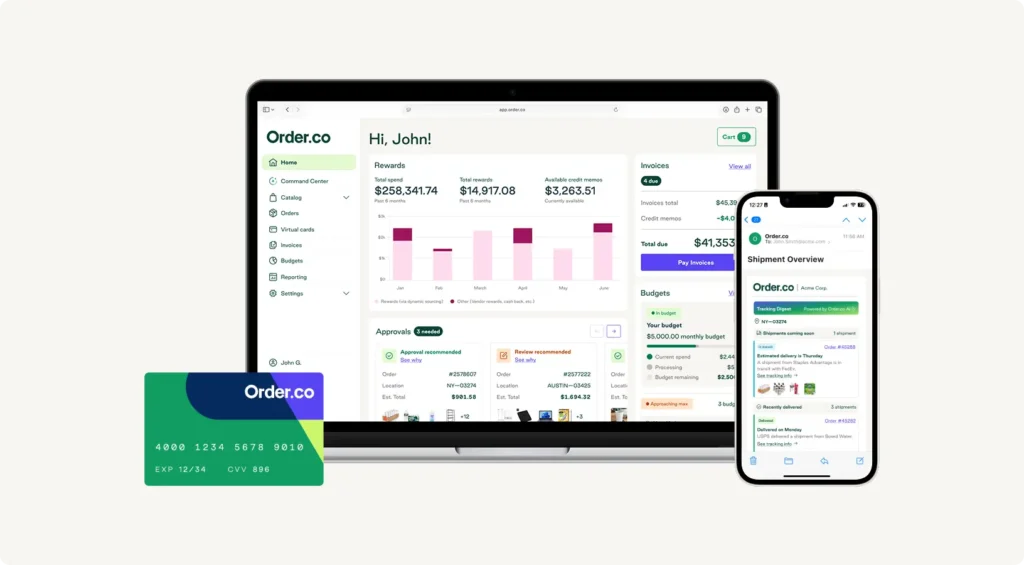

Best for spend control & automation: Order.co

Order.co is an AI-powered procurement and finance automation platform that includes vendor-locked virtual cards. Eligibility is based on the business's cash flow and banking activity, so fair-credit applicants who can demonstrate healthy cash flow can qualify regardless of personal credit score.

Key features:

- Vendor-locked virtual cards that automatically restrict each card to a single approved merchant.

- Per-card spend limits and expiration dates for one-time projects or recurring vendor payments.

- Line-item GL coding on every transaction, which makes month-end reconciliation faster and more accurate than transaction-level coding.

- Up to 37 days to pay on purchases, giving you more working capital than standard Net 30 terms.

Best for: Multi-location procurement and finance teams that want spend controls, working capital, and procurement automation in a single platform.

Considerations: Pricing is not publicly available, so onboarding involves a sales conversation.

Best for 1% cashback & no annual fee: Capital One Spark 1% Classic

Capital One's Spark 1% Classic is a reliable unsecured card for fair-credit applicants. It supports credit-building by reporting to major bureaus and pairs straightforward rewards with no annual fee.

Key features:

- Annual fee: $0

- Rewards: 1% cash back on every purchase, unlimited; 5% cash back on hotels and rental cars booked through Capital One Travel

- APR: 28.99% variable

- Reports to: Major business credit bureaus

Best for: Fair-credit businesses that want a simple unsecured card with consistent rewards and credit-building support.

Considerations: The variable APR is high, so this card is better for those that pay in full each month rather than carrying a balance. The 1% cash back rate also sits below the 1.5% common on cards for stronger credit profiles.

Best for revenue-based approval: Capital on Tap Business Credit Card

Capital on Tap underwrites based on both personal credit and business revenue, which can make it accessible to fair-credit applicants with steady monthly cash flow.

Key features:

- Annual fee: $0

- Rewards: 1.5% cash back on all spend; 2% with weekly autopay enabled

- Credit limit: Up to $50,000

- APR: 16.74%–86.24% variable, based on creditworthiness

- Fees: No foreign exchange fees, no ATM fees

- Eligibility: LLC or corporation only (no sole proprietors); minimum $2,500/month in revenue

Best for: Fair-credit businesses with consistent revenue that want a higher potential credit limit and flat-rate rewards.

Considerations: Eligibility is restricted to LLCs and corporations earning at least $2,500 per month, which excludes sole proprietors and very early-stage startups. The APR range is wide, and fair-credit applicants typically land at the upper end rather than the advertised starting rate.

Best secured options: Bank of America & FNBO

Secured credit cards are the most reliable path for businesses early in their credit journey. Two cards stand out for fair-credit applicants:

1. Bank of America Business Advantage Unlimited Cash Rewards Mastercard offers cash-back rewards on a secured business credit card, which is uncommon in the category.

Key features:

- Annual fee: $0

- Rewards: 1.5% cash back on every purchase, unlimited

- Minimum deposit: $1,000

- APR: 16.74%–26.74% variable

- Reports to: Business credit bureaus only

Best for: Businesses that already bank with Bank of America and want the Preferred Rewards tier boosts on top of standard cash back while building business credit.

Considerations: Reports only to business credit bureaus, so it won't move your personal FICO. The cash-back rate is most valuable in combination with a $20,000+ BoA business banking balance, which unlocks the Preferred Rewards tier boosts.

2. FNBO Business Edition Secured Mastercard pays interest on your security deposit, a feature most secured business credit card issuers don't offer.

Key features:

- Annual fee: $39

- Rewards: Mastercard Easy Savings automatic rebates

- Deposit range: $2,000–$10,000 (held in an interest-bearing account; determines your credit limit, subject to approval)

- APR: 24.24% variable

- Reports to: Business and personal credit bureaus

Best for: Businesses focused on building both personal and business credit, with enough liquidity to put down $2,000+ and benefit from the interest-bearing deposit.

Considerations: Carries a $39 annual fee and offers no ongoing cash-back rewards beyond Mastercard Easy Savings rebates. The higher minimum deposit also raises the entry bar for businesses with tighter cash flow.

Best for no personal credit check: Ramp & BILL Divvy

For fair-credit businesses with healthy cash flow, the two corporate charge cards below can be a faster route to a working business card than waiting for credit to improve. Both underwrite business cash flow and banking history, skip personal credit checks, and don't typically report to personal credit bureaus, so they won't help build personal credit, but they also won't be blocked by a fair-credit score. Both require full balance payoff each billing cycle.

1. Ramp Corporate Card focuses on automation, expense controls, and AI-powered spend insights, paired with one of the largest partner-discount programs in the category.

- Annual fee: $0

- Card type: Charge card (pay in full each billing cycle); no APR

- Rewards: Up to 1.5% cash back (exact rate set by Ramp based on business profile)

- Partner discounts: $350K+ in credits across AWS, UPS, Amazon Business, and 100+ partners

- Eligibility: Corporation, LLC, or limited partnership; at least $25,000 in a US business bank account; most operations and spend based in the US

- Reports to: Does not report to personal or business credit bureaus, so the card itself won't build credit history of either type

Best for: Incorporated businesses with at least $25,000 in cash reserves that want expense automation and partner discounts alongside a corporate card.

Considerations: The 1.5% rewards rate is a maximum, not a guarantee. Your actual rate is set by Ramp after approval and may be lower. Sole proprietors aren't eligible. As a charge card, it doesn't support carrying a balance, which can be a fit issue for fair-credit businesses that occasionally need to.

2. BILL Divvy Card pairs a corporate charge card with a budgeting platform and a tiered rewards program built around payment frequency.

- Annual fee: $0

- Card type: Charge card; credit line from $1,000 to $5M, based on business cash flow

- Rewards: Tiered points program; weekly payers earn up to 7x on restaurants, 5x on hotels, 2x on recurring software; monthly payers earn 1x on most eligible purchases; bonus categories cap at the first $5,000 of monthly spend

- Eligibility: LLC, corporation, or partnership (sole props can apply but most approvals favor incorporated businesses); approximately $20,000+ in monthly revenue or bank balance recommended

- Reports to: Small Business Financial Exchange (which may share with business credit bureaus); does not report to personal credit bureaus

Best for: Businesses with consistent monthly spend and the cash flow to pay weekly or semi-monthly, who also want strong budgeting controls alongside the card.

Considerations: Rewards require spending at least 30% of your credit limit each month, and accumulated points can be forfeited for inactivity, missed monthly payments, or account closure within the first year. Points also can't be redeemed during the first 12 months. Monthly-only payers earn meaningfully less than the headline rates suggest.

How to choose a business credit card with fair credit

For businesses with fair credit, the right card matches the way your business actually spends and the credit profile you want to build over time. Approval is the floor, not the goal.

Factors to evaluate:

- Secured vs. unsecured. Unsecured cards avoid the deposit and offer faster access to a credit line, while secured cards trade easier approval for tied-up cash and stronger credit-building impact.

- Credit reporting. Cards that report to business and personal credit bureaus build your business credit score over time. No-credit-check corporate cards typically don't report, so they're better suited to operations than credit-building.

- Rewards. Calculate whether the rewards rate generates enough return on your spend mix to be worth chasing. Flat rates are simpler to project; tiered programs need consistent category spend to deliver their advertised value.

- Total cost. Add up annual fees, foreign transaction fees, and APR exposure (if you ever carry a balance). A card with a $39 annual fee can still net out positive if it's also paying interest on a security deposit or supporting your credit rebuild.

- Limits and growth. Confirm the starting limit meets your operating needs and check whether spending limits scale based on payment history. For fair-credit businesses, growth potential often matters more than the day-one ceiling.

- Operational features. For multi-location and finance-team-led businesses, employee cards, expense management tools, accounting software integrations, and purchasing controls can deliver day-to-day value alongside whatever card you carry.

If rebuilding credit is your top goal, prioritize secured cards that report to bureaus. If your business relies on a credit card to cover operating expenses—the most common reason firms sought financing in the Federal Reserve's 2026 Report on Employer Firms (cited by 56% of applicants)—a no-credit-check corporate card may deliver more value than rewards optimization alone. Either path depends on a clear sense of how the card is actually being used.

Choose the Right Procurement Technology With This Decision Matrix

Find 15 must-ask questions to narrow down your software search and make your research process MUCH easier.

"*" indicates required fields

Reduce spend risk and protect cash flow while you build credit with Order.co

For businesses navigating fair credit, the way you spend affects your credit score more than the type of card you choose.

If unapproved spending is pushing your card balance past healthy utilization, a spend management platform like Order.co can help you control spend at the point of purchase, while flagging savings opportunities. After switching ot Order.co, CorePower Yoga, a 200+ location fitness chain, reduced monthly unapproved spend from $50,000 to zero while capturing another $11,000 a month in product savings through AI sourcing.

If new investments are straining the cash reserves you need to pay your card on time, consider tools that give you breathing room on large expenses without taking on more debt. Silver Therapeutics, a multi-state cannabis retailer, used Order.co's working capital tools to fund new store construction without burning through cash.

Improving fair credit takes more than the right card. A business credit card can build credit history and earn rewards on your spend, but it doesn't change the spend behavior that affects your score in the first place.

Book a demo to see how Order.co helps you control spend, capture savings, and ease cash flow pressure while you build credit.

FAQs about business credit cards for fair credit

Yes. Fair credit (FICO 580–669) qualifies you for business credit cards, though your options are narrower than for good or excellent credit. Most fair-credit applicants qualify on the upper end of the range (640+), and approval often depends on factors beyond the FICO score: business revenue, banking history, and how long the business has been operating. Secured cards offer an easier path at the lower end of fair credit, and no-credit-check corporate cards underwrite the business directly without pulling your personal score at all.

Show 6 to 12 months of consistent business banking activity before applying, and choose cards designed for fair-credit applicants rather than general business cards. Steady deposits, healthy cash flow, and low existing debt often weigh as much as the personal FICO score, especially with providers that underwrite business revenue alongside credit.

Use the card consistently and pay it off in full each month. Payment history accounts for 35% of your FICO score, making on-time payments the highest-impact lever. Keep card utilization below 30% of your limit to protect the second-largest factor (amounts owed, 30% of score). Keep older accounts open even after you qualify for better cards, because credit history length contributes 15% of your score.

Get started

Schedule a demo to see how Order.co can simplify buying for your business.

"*" indicates required fields