Comparing The Best Cash Back Business Credit Cards (2026)

Comparing The Best Cash Back Business Credit Cards (2026)

Cash back business credit cards turn the money your business already spends into ongoing rebates, but the headline rates only tell part of the story. If your finance team is chasing receipts, flagging off-policy purchases, and reconciling multiple cards across locations every month-end, those rewards rarely net out positive against the manual work surrounding them.

Choosing the right card means weighing options against your unique spend profile, and recognizing when a spend management platform delivers more by giving you visibility before purchases happen, recovering AP time at close, and surfacing hard-dollar savings the card itself can't reach.

Key takeaways: cash back business credit cards

- Annual fees, redemption mechanics, and spending category caps usually matter more than headline cash back rates.

- The right card depends on where your spend lands, whether you carry a balance, and how you weigh welcome offers against ongoing earn rate.

- Flat-rate cards win on simplicity; category cards win on returns when spend is concentrated enough to clear the bonus thresholds.

- Stacking multiple cards stops paying off when managing them becomes a tax on your finance team's time.

- Order.co's procurement platform complements the right cash back card with hard-dollar savings from AI-sourcing, upstream control on every purchase, and recovered AP time at month-end.

Download the free ebook: Choose the Right Procurement Technology With This Decision Matrix

What is a cash back business credit card?

A cash back business credit card returns a percentage of every qualifying purchase as cash, statement credit, or direct deposit. The reward comes back either as a flat rate across all spend (commonly 1.5% or 2%) or as elevated rates in specific business expense categories like office supplies, telecom, fuel, and travel.

Business cash back rewards typically pay in dollars rather than points or miles, which makes them simpler to reconcile and easier to deploy back into operations.

For a single-location business, the appeal is straightforward. You turn money you already spend into a small ongoing rebate. For multi-location business owners, the math gets more complicated. Issuing cards to general managers and regional directors creates a labor cost downstream: hours spent matching receipts, chasing missing expense reports, and reconciling statements across locations at month-end.

How to choose the right cash back business credit card

Choosing the right card type depends on your answers to three questions, which determine your spend profile.

- Where does most of your monthly spend land? If half or more of your spend concentrates in one or two categories (office supplies, fuel, internet, phone, restaurants), a category bonus card usually wins. If spend is distributed evenly across your business, a flat-rate card is simpler and often nets out higher.

- Do you carry a balance, or pay in full each month? If you pay in full, the variable APR is irrelevant, and you can focus on rewards rates, fees, and welcome bonuses. If you carry a balance, a 0% intro APR card saves more in deferred interest than any rewards program returns.

- What are you optimizing for: welcome bonus, ongoing earn rate, or zero annual fee? Welcome bonuses are one-time wins ($500 to $2,000 for hitting a spend threshold in the first few months). Earn rates compound over each calendar year. Annual fees can be worth paying for high-volume spend, but under $200,000 in annual card spend, a no-fee card with a strong flat rate is usually the better bet.

Statement credits reduce your balance owed but never appear as cash. Direct deposits land in your business checking account and can be deployed as working capital. Checks are the slowest and least flexible. If you're optimizing for cash flow, redemption flexibility matters as much as earn rate.

If your spend is distributed across many categories and your finance team is already managing multiple cards across locations, the bigger question isn't which card to add, but whether the workflow around your cards is costing you more than the rewards return. That's the layer a spend management platform addresses, separately from cash back rates.

Choose the Right Procurement Technology With This Decision Matrix

Find 15 must-ask questions to narrow down your software search and make your research process MUCH easier.

Comparing top cash back business credit cards (2026)

The cards below include top options across the most common business spend profiles. Use the three-question framework above to narrow your choice, then compare against the table.

| Card | Annual fee | Welcome bonus | Introductory APR | Variable APR | Rewards rate | Credit score needed |

| Chase Ink Business Unlimited | $0 | $750 after $6,000 in 3 months | 0% for 12 months | 16.74% to 24.74% | 1.5% unlimited | Good to excellent |

| Chase Ink Business Cash | $0 | $750 after $6,000 in 3 months | 0% for 12 months | 16.74% to 24.74% | 5% on office supplies, internet, cable, and phone (first $25k/yr); 2% on gas and dining (first $25k/yr); 1% on the rest | Good to excellent |

| AmEx Blue Business Cash Card | $0 | $250 statement credit after $3,000 in 3 months | 0% for 12 months | 16.74% to 28.49% | 2% on first $50k/yr; 1% on the rest | Good |

| Capital One Spark Cash Plus | $150 | $2,000 after $30,000 in 3 months | None | None (pay in full) | 2% unlimited | Excellent |

| U.S. Bank Triple Cash Rewards Visa | $0 | $750 after $6,000 in 180 days | 0% for 12 months | 17.24% to 26.24% | 3% on gas, restaurants, office supplies, and phone (uncapped); 1% on the rest | Good to excellent |

| Wells Fargo Signify Business Cash | $0 | $500 after $5,000 in 3 months | 0% for 12 months | 16.74% to 24.74% | 2% unlimited | Excellent |

| Bank of America Business Advantage Customized Cash Rewards | $0 | $500 after $5,000 in 90 days | 0% for 7 billing cycles | 16.74% to 26.74% | 3% on category of choice and 2% on dining (combined $50k/yr cap); 1% on the rest | Good to excellent |

Which card is right for your spend profile?

Understanding your spend profile lets you match your situation to the right card. Here’s a quick guide:

- Chase Ink Business Unlimited: Best for flat-rate simplicity at scale. Unlimited 1.5% with no annual fee, 12-month 0% intro APR, and a $750 welcome bonus that's among the largest available for a no-fee card.

- Chase Ink Business Cash: Best for concentrated category spend. The 5% rate on office supplies, internet, cable, and phone services is one of the highest category bonuses available with no annual fee, with a separate 2% rate on gas and dining. Each bonus pool caps at $25,000 in annual spend.

- American Express Blue Business Cash Card. Best for newer or smaller businesses. The 2% rate on the first $50,000 in annual spend fits businesses not yet at six-figure card volume, and AmEx often considers applicants based on owner personal credit when the business itself doesn't have an established history.

- Capital One Spark Cash Plus: Best for high-volume spenders. The $150 annual fee earns back quickly at scale, the $2,000 welcome bonus is the largest standard public offer in this comparison, and an additional $2,000 bonus is available for every $500,000 spent in the first year. No preset spending limit.

- U.S. Bank Triple Cash Rewards Visa: Best for uncapped no-fee category bonuses. The 3% rate on gas, restaurants, office supplies, and phone services applies to all qualifying spend rather than capping at a category threshold.

- Wells Fargo Signify Business Cash: Best for no-fee flat-rate spend. Unlimited 2% with no annual fee, simplest to manage when spend is distributed across categories.

- Bank of America Business Advantage: Best for shifting spend patterns. You can change the 3% bonus category once per month (gas stations, office supply stores, business travel, and others), which is useful when spend patterns change seasonally.

Why teams should look beyond cash back rates alone

Cash back returns a percentage of spend your business is already making, but at multi-location scale, the bigger question is whether the workflow around your cards is costing more than the rewards earn back.

The hidden cost of card-based workflows shows up in:

- Reconciliation tax at month-end. Every card transaction has to be matched to a receipt, coded to a GL account, and filed for audit. At 20 locations with 10 cardholders each, that's 200 monthly statements to reconcile before actual close work begins.

- Off-policy purchases. A card approved for office supplies might be used for premium-brand items, personal purchases, or things that would never have been approved if reviewed individually. Without line-item visibility, those purchases blend into the statement and slip through unnoticed.

- Rogue spend and overstock. Traditional credit cards have no upstream approval. A general manager can order $2,000 of supplies on a Tuesday with no one reviewing it until the statement arrives.

A spend management platform addresses these gaps with upstream controls built into purchasing, line-item visibility at the moment of sale, and AI-driven sourcing that surfaces price differences cards can't see. Customers using Order.co capture around 5% in hard-dollar savings through AI sourcing alone, more than double the headline rate of most cash back cards.

Choose the Right Procurement Technology With This Decision Matrix

Find 15 must-ask questions to narrow down your software search and make your research process MUCH easier.

"*" indicates required fields

How Order.co complements the right cash back card

Order.co is an AI-powered procurement, AP automation, and spend management platform built for multi-location operators. The platform doesn't earn cash back the way a credit card does. Instead, it replaces the manual workflow that surrounds card-based purchasing, including expense reports, statement reconciliation, and after-the-fact spend visibility. Alongside the right card, you keep earning rewards while removing operational drag.

With Order.co, teams get:

- Curated catalogs. You select the vendors and products your team can access, so the easiest path to purchase is also the approved one. Choose from Order.co’s 40,000+ supplier network or bring your own vendors into the platform.

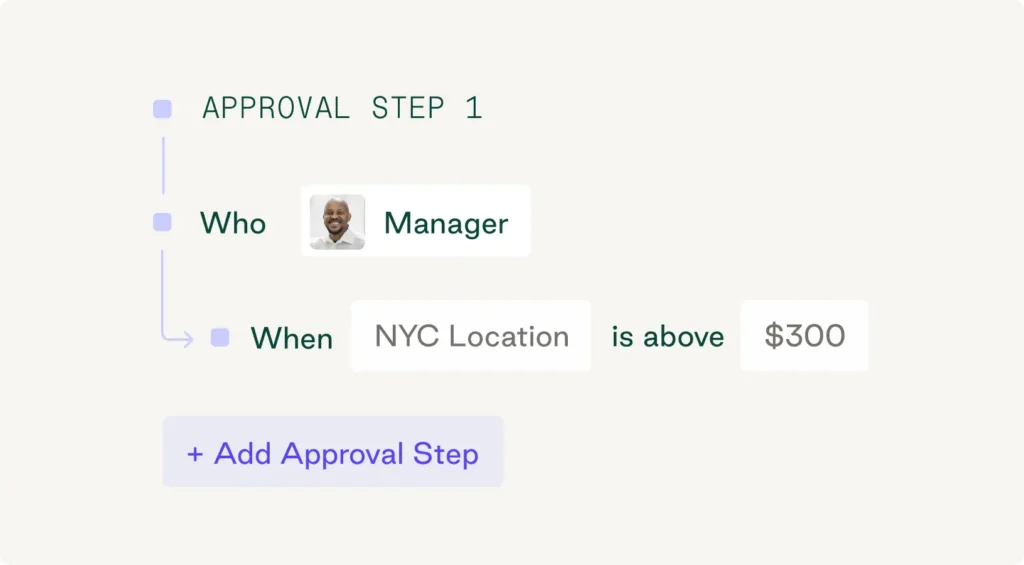

- Automated purchasing workflows. Purchase requests route through configurable approval workflows by user, amount, location, or product category, with real-time budget caps to prevent overspend. Recurring orders ship automatically on the cadence your team sets.

- Virtual cards. Issue unlimited vendor-locked virtual cards for online and recurring purchases. Cards lock to a specific vendor for built-in fraud protection, and every transaction syncs with line-item visibility and your approval workflows.

- AI-powered sourcing and insights. The sourcing algorithm finds the best price or sources alternatives when products are out of stock. Anomaly detection flags spend that deviates from established patterns before it hits the statement.

- Line-item visibility on every transaction. Finance sees exactly what was bought, by whom, and against which budget, at the moment of purchase.

- Customized billing. With weekly invoicing and Net 30 terms, for example, you have up to 37 days to pay, improving cash flow and visibility into what you owe and when.

Order.co customer TOCA Football, a sports entertainment company with 44 facilities and 210+ employees, brought 99.5% of purchases under approval control after replacing card-based ordering with the platform. Concession supply orders that used to arrive as overstock and out-of-date products now route through a regional director review. Custom-branded soccer balls ship to every facility on a four-month cadence, with no one placing an order, and individual expense reports across locations disappeared.

Pair the right card with the right purchasing system

The right cash back card depends on your spend profile, whether your business pays in full or carries a balance, and what you're trying to optimize for (welcome bonus, ongoing earn rate, or zero annual fee). For a single-location business or a team with simple purchasing needs, choosing the right card is the entire decision.

For multi-location operators, the decision isn't just about which card offers the most cash back. It's about pairing the right card with a system that provides visibility upstream, keeps purchases on policy by default, and surfaces savings opportunities inside the workflows your team actually uses.

Schedule a demo to see how you can simplify purchasing and speed up month-end close while earning cash back rewards.

FAQs about cash back business credit cards

For mixed-category everyday spend, a flat-rate 2% card with no annual fee is usually the best fit. Look for one that pairs unlimited or high-cap cash back with a 0% introductory APR period, which protects cash flow in the first year. For multi-location operators, the bigger return often comes from pairing the right card with a spend management platform like Order.co that gives finance visibility upstream, surfaces hard-dollar savings through AI sourcing, and recovers AP time at month-end.

Yes, though the options narrow. Issuers underwrite business cards on a combination of business revenue and the owner's personal credit, so newer businesses without credit history often qualify based on the owner's credit score alone. Some issuers are more accommodating to newer entities, particularly cards with no annual fee and lower minimum spend requirements. Secured business cards are an alternative if you don't yet qualify for unsecured credit.

Cash back is most often redeemed as a statement credit, a direct deposit, or a check. Some issuers also offer gift card or partner-rewards redemption, but these typically deliver less per-dollar value than the cash options. Direct deposit is generally the most flexible because the funds become working capital you can deploy elsewhere, while statement credit just reduces next month's balance.

Get started

Schedule a demo to see how Order.co can simplify buying for your business

"*" indicates required fields