Retail Cash Flow Management: Complete Guide for 2026

Retail Cash Flow Management: Complete Guide for 2026

Retail runs on thin margins and constant motion. You pay for inventory weeks before it sells, cover rent and payroll on a fixed schedule, and watch revenue swing depending on the season. A store can seem profitable on paper yet still run short on cash when income and expenses fall out of sync.

Bridging that gap is the job of retail cash flow management. For finance and operations leaders running multiple locations, it comes down to three things working together:

- Forecasting that surfaces shortfalls before they arrive

- Operational controls over how and what teams buy

- Technology that provides visibility across every store and vendor

Balancing these levers turns cash flow from a weekly guessing game into a predictable growth asset.

Quick answer:

- Retail cash flow problems usually come down to timing. You pay for inventory long before the revenue from those sales comes in.

- The most common pressures are rising operating costs, unpredictable demand, and uneven vendor payment terms. Each one ties back to working capital management.

- Improving cash flow requires a multi-pronged approach that connects purchasing approvals, spend controls, net terms, and inventory planning.

- A 13-week cash flow forecast gives finance teams week-by-week visibility into inflows and outflows, so shortages get spotted early enough to act on.

- Order.co centralizes purchasing, approvals, and vendor payments in one platform so multi-location retailers have the visibility and control necessary to protect cash before it leaves the business.

Download the free tool: Financial Projections Template

What is retail cash flow management?

Retail cash flow management is the practice of tracking, forecasting, and controlling when cash moves in and out, so you always have enough on hand to cover your obligations. It covers the full cycle: buying inventory, collecting sales revenue, paying vendors, and timing each to protect your cash balance.

Cash flow and profitability are separate questions. A retailer can post healthy profit margins and still hit a cash shortage because money leaves the business to pay for inventory weeks or months before that inventory sells and the revenue lands. Effective cash flow management keeps those timing gaps from turning into missed payroll or late vendor payments.

Financial Projections Template

Download the financial projections template to clarify financial patterns, track spending throughout the year, and make better-informed decisions about the future.

What are the biggest retail cash flow challenges?

Most retail cash flow problems stem from a handful of recurring pressures, with rising costs at the top of the list. At the end of 2025, 45% of small business owners named inflation as their biggest challenge, according to the US Chamber of Commerce Small Business Index. In addition, 77% of small employer firms reported facing rising operating expenses, tariff-related cost challenges, or both in the Federal Reserve's 2025 Small Business Credit Survey.

Here's how the most common challenges can impact your cash position:

| Challenge | Direct cash flow impact | Working capital pressure |

| High operating costs | Rent, payroll, and utilities need to be paid, even when sales dip | Less cash left to fund inventory and growth opportunities |

| Unpredictable demand | Overstocks freeze cash in unsold goods; stockouts force costly rush orders | Capital gets tied up in unsold inventory or lost to premium pricing |

| Uneven vendor terms | Paying vendors before collecting sales revenue creates short-term cash gaps | Cash reserves get stretched thin when due dates overlap |

| Unexpected expenses | Repairs and missed shipments trigger unplanned spending | Emergency outflows eat into your cash buffer |

| Supply chain disruptions | Delivery delays push you toward early or duplicate ordering | Cash commitments come earlier than planned |

These pressures compound across locations, which is why managing retail risk and a steady retail supply chain are vital to protecting cash.

How to improve retail cash flow management

No single tactic fixes retail cash flow. You can improve it by pulling several levers at once, controlling what your teams buy, planning repayments, and keeping inventory levels in line with demand.

The four strategies below work together. Tighter purchasing feeds better forecasting, and better terms give you room to act on both.

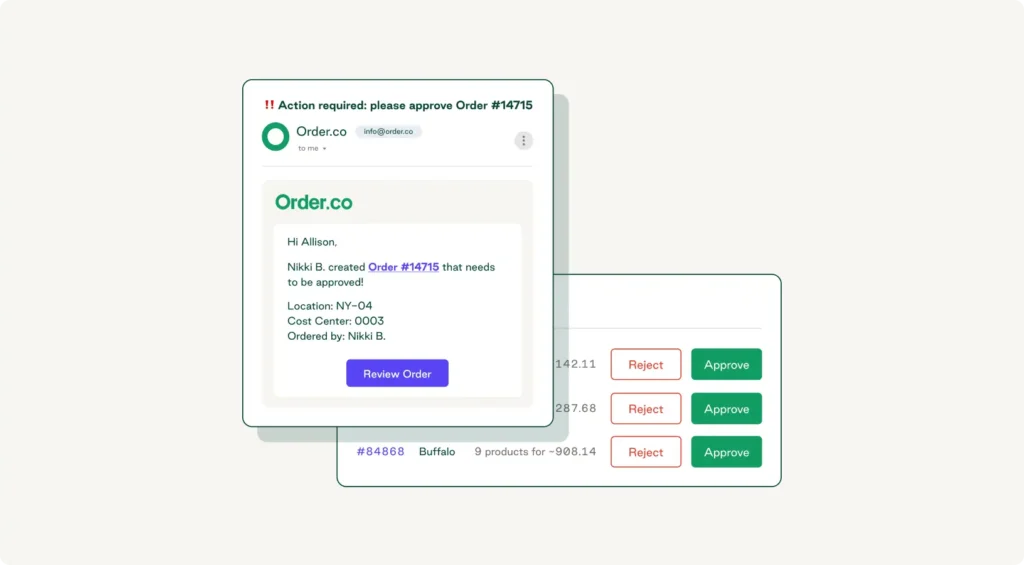

1. Build approvals into the purchasing process

Controlling where your money goes starts before orders are placed. An approval step routes every purchase to the right person, whether that's a store manager, a regional director, or a finance lead, so spending matches policy and budget from the beginning.

Approvals also catch the small leaks that compound over time, like duplicate orders, off-policy vendors, and quantities that outpace actual demand. Order.co builds approvals directly into the purchasing workflow, so a manager's order gets reviewed and adjusted before it ever reaches the vendor.

2. Control supplies spending

With a strong approval process in place, the next lever is controlling how much gets spent and on what, starting at the catalog level. When only pre-approved products and vendors are visible to buyers, compliant purchasing becomes the default path rather than something you have to enforce after the fact.

From there, you can set spending limits by location or category, cap who can buy and how much, and put guardrails around indirect spend like packaging, cleaning supplies, and office goods. Order.co provides these controls and full spend visibility in one place, so no single region can exceed its supply budget.

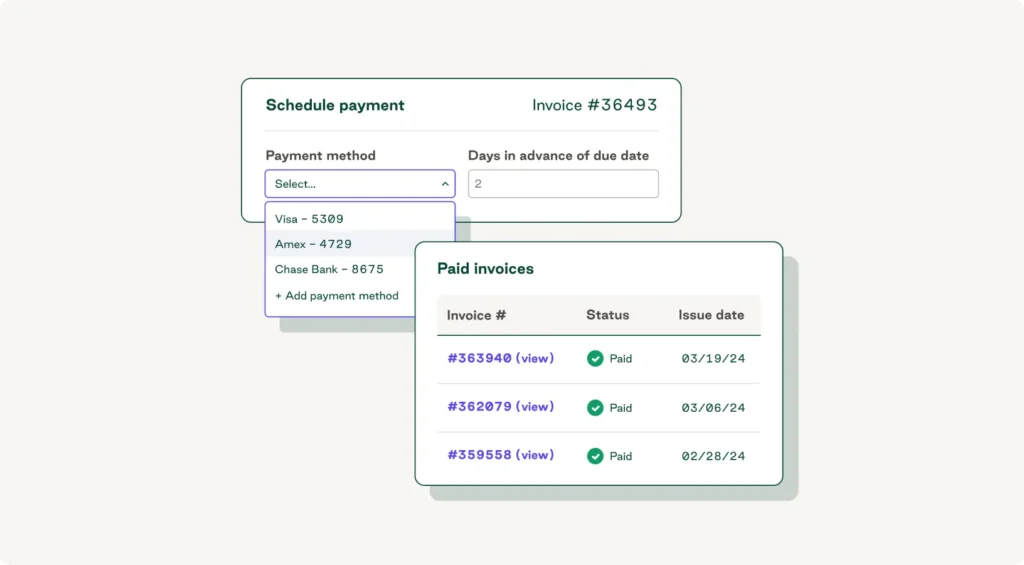

3. Negotiate better net terms

Vendor payment timing is one of the most effective levers for managing cash. Negotiating longer net terms of 30, 60, or 90 days keeps money in your account longer and provides a buffer during slow sales periods.

Treat days payable outstanding (DPO) as a financial planning metric. A higher DPO tells you how long you can hold cash before it's due, which feeds directly into your forecast. When reserves are healthy, early payment discounts become a useful secondary lever, and capturing terms like 2/10 net 30 can cut supply costs meaningfully at scale. Pairing better terms with broader payment optimization strategies protects working capital without straining supplier relationships.

4. Avoid supply over- and understocks

Both overstocking and understocking hurt cash directly. Buy too much, and capital sits frozen in product on the shelf. Run short, and you pay premium prices for rush orders or lose the sale entirely. The goal is keeping enough of what sells without locking cash into what doesn't.

Purchasing controls do a lot of the work here. When TOCA Football scaled to dozens of locations, managers ordering concession supplies directly through vendor sites kept ending up with overstock and out-of-date products. After moving purchasing onto Order.co, approval workflows let the team catch and trim oversized orders before they shipped, and recurring orders kept high-use items stocked automatically.

Seasonal planning matters too. Build inventory ahead of peak demand, but tie those buys to forecasted sales and your broader inventory planning. TOCA concentrates roughly a third of its annual spend in its winter peak, and centralized reporting by location and category helps the team prepare without overcommitting cash.

How to build a 13-week cash flow forecast for retail

These levers work better when you can see their impact ahead of time. A 13-week cash flow forecast gives finance teams a rolling view of expected inflows and outflows over the next quarter. It's long enough to catch a shortfall and short enough to stay accurate.

Here's how to build one.

1. Map your weekly cash inflows by channel

Start with the money you have coming in. Break expected sales out by channel: in-store, ecommerce, and wholesale, and plot it week by week. Lean on recent sales data and known trends so each week reflects what you'll actually collect rather than an average.

2. Schedule fixed and variable outflows against your AP calendar

Next, map your outflows against the same timeline. Fixed costs like rent, payroll, and loan payments land on predictable dates. Variable expenses, such as inventory and supplies, follow your accounts payable calendar and vendor terms. Lining payments up against due dates shows exactly when liquidity gets tight.

3. Layer in seasonality, promotions, and inventory receipts

Retail cash flow isn't flat. Adjust each week for seasonal fluctuations, planned promotions, and the timing of large inventory receipts. The weeks you pay for holiday stock often land well before those sales arrive, so mapping those buys in advance keeps a big payment from catching you off guard.

4. Run best, base, and worst-case scenarios

Build three versions: a base case on your best estimate, a worst case with slower sales and higher costs, and a best case with upside. Comparing them shows how much cushion you have and when you'd need to act, whether that's pulling back orders, adjusting terms, or tapping a line of credit before a gap becomes urgent.

Financial Projections Template

Download the financial projections template to clarify financial patterns, track spending throughout the year, and make better-informed decisions about the future.

"*" indicates required fields

How a centralized spend management platform supports retail cash flow management

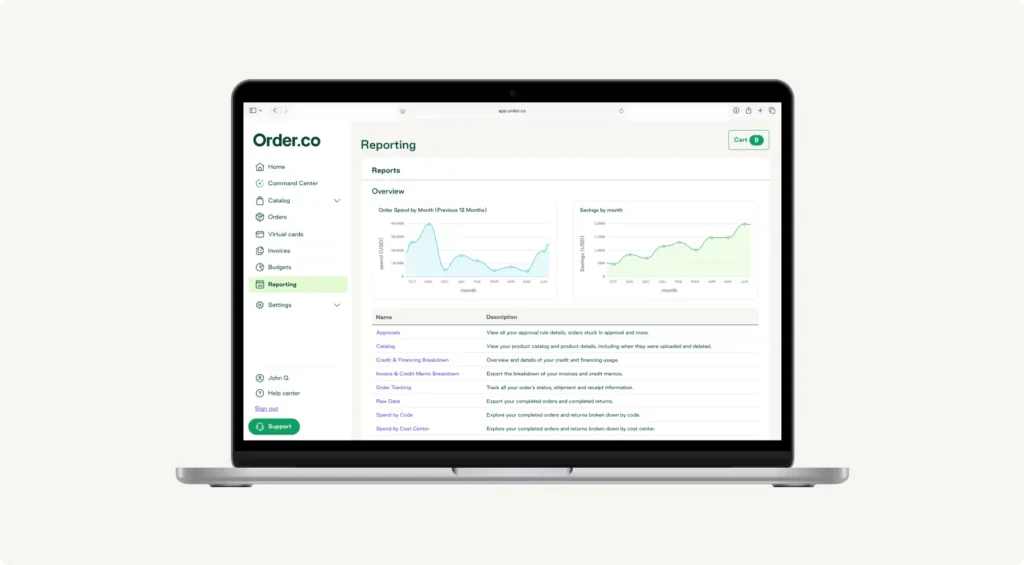

A forecast is only as good as the data behind it, and manual tracking breaks down as a retail operation grows. Spreadsheets pulling from separate vendor logins, company cards, and store-level records leave gaps exactly where you need accuracy, in what's been committed, what's been paid, and what's still owed.

A centralized spend management platform closes those gaps. When purchasing, approvals, vendor commitments, and payment timing live in one place, you get a real-time view of cash outflows instead of a month-old reconstruction. That visibility is what makes forecasting reliable and lets you act on the levers above before problems compound.

A retail management platform like Order.co also puts AI to work in everyday buying, with a sourcing algorithm that finds the best price and surfaces options when an item goes out of stock, so cost control runs in the background of every order.

Building healthy cash flow with Order.co

Healthy retail cash flow comes down to controlling spend before it happens and having clear visibility into it afterward. Order.co connects both across every location:

- Uncontrolled, off-policy buying. Curated catalogs and approval workflows keep purchases aligned to budget and policy from the first click, so rogue spend doesn't drain cash.

- Overstock and rush orders. Pre-approved product lists and recurring orders keep high-use items in stock and oversized orders in check.

- Cash tied up in vendor payments. Order.co pays your vendors via their preferred method, Net 1, and rolls those payments into customized bills that fit your bookkeeping, giving you predictable timing instead of scattered due dates.

- No clear view of spend. Line-item purchasing data and real-time budgets show finance exactly where cash is going, by location, category, and vendor.

For retailers managing growth, that combination protects working capital while keeping retail operations stocked and teams moving. See what a real-time view of every location's spend does for your cash position. Schedule a demo of Order.co.

FAQs about retail cash flow management

A 13-week cash flow forecast is a rolling, week-by-week projection of the cash entering and leaving your business over the next quarter. Retailers use it because it covers a full quarter of seasonality and vendor payment cycles while staying short enough to stay accurate. It gives finance teams enough warning to spot a shortfall and act, whether by adjusting orders, terms, or financing, before a tight week turns into a missed payment.

Start with the levers you have direct control over. Tighten purchasing approvals to stop off-policy and duplicate orders, renegotiate vendor terms to hold cash longer, and pause non-essential buying until reserves recover. Increasing inventory turnover through markdowns also frees up cash quickly. These moves work faster than waiting on sales growth, because they change the timing of money leaving your business rather than relying on more coming in.

Inventory ties up cash between the moment you pay a vendor and the moment a product sells. Buy too much and that cash sits frozen on the shelf; buy too little and you lose sales or pay premium prices for rush orders. Aligning purchases with forecasted demand keeps cash moving instead of stuck, which is why inventory decisions have such a direct effect on a retailer's available cash.

Get started

Schedule a demo to see how Order.co can simplify buying for your busines

"*" indicates required fields