B2B BNPL Explained: How Buy Now Pay Later Works for Business

B2B BNPL Explained: How Buy Now Pay Later Works for Business

If your business makes large or recurring purchases, paying the full invoice on day one ties up cash you could be putting toward growth. B2B buy now, pay later (BNPL) lets you take delivery now but spread the cost over weeks or months, giving your procurement and finance teams more room to manage cash flow.

Learning how B2B BNPL works, how it stacks up against trade credit and corporate cards, and which providers lead the market can make it easier to decide whether it fits your purchasing strategy.

Quick answer:

- B2B BNPL lets you buy now and pay over time through installments or extended net terms, freeing up working capital for large or recurring purchases.

- It works much like trade credit but with faster approval, because a third-party provider underwrites the buyer and provides the seller with upfront payment.

- Most B2B BNPL providers offer net 30–90 day terms and don't require a personal guarantee, which makes approval easier than opening a traditional credit line.

- Demand is climbing fast. The global B2B BNPL market is projected to reach $466.6 billion by 2030, growing at a 17.1% CAGR.

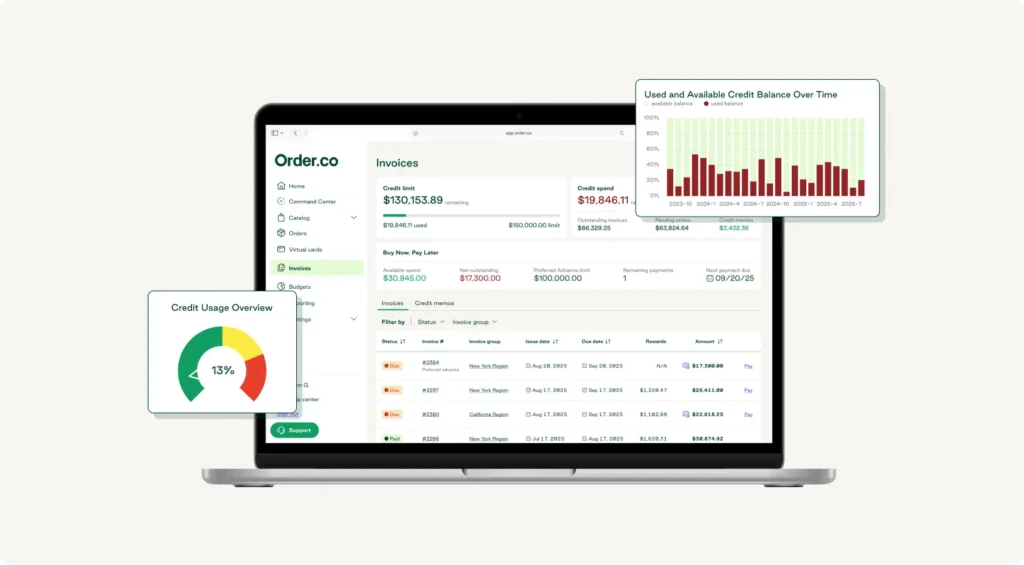

- Order.co offers B2B BNPL, flexible net terms, and virtual cards inside a single procurement and finance platform, giving you flexible payment options without juggling a separate BNPL lender or opening another credit card.

Take Advantage of B2B BNPL with Order.co Financial Offerings

What is B2B BNPL?

B2B buy now, pay later is a payment option that lets your business buy goods or services immediately and pay for them later, either in installments or on extended net terms. A third-party provider pays the seller up front and then collects money from the buyer over an agreed schedule.

Buyers benefit by gaining access to inventory, equipment, and supplies without draining cash reserves on the day of purchase. Sellers benefit because the provider assumes the credit risk and pays at the point of sale, helping vendors get paid quicker.

The model grew out of consumer BNPL but solves different problems:

- B2B purchases are typically larger.

- Approval involves more stakeholders.

- Buyers usually expect credit terms as standard.

BNPL offers predictable B2B payments and flexible financing, leaving more room to manage cash flow.

B2B BNPL with Order.co Financial Offerings

Unlock capital advances of up to $500k, net terms for all vendors and virtual cards with Order.co, an easy and affordable partner for your business’s growth.

B2B BNPL companies

A handful of providers dominate the B2B BNPL space, and they differ in who they serve, the terms they offer, and where they operate. Here's how five of the most established options compare.

| Provider | Best for | Net terms offered | Personal guarantee | Industries served |

| TreviPay | Enterprise and marketplace trade-credit programs | Net 15-90 days | Typically not required | Manufacturing, retail, marketplaces, global enterprise, transportation |

| Resolve | US mid-market sellers adding net terms at checkout | Net 30, 60, or 90 days | Typically not required | Wholesale, manufacturing, distribution |

| Balance | B2B marketplaces and digital-first sellers | Net terms or installments (up to 60 or 90 days) | Not required | Marketplaces, ecommerce, wholesale |

| Mondu | European and cross-border sellers | 30, 45, 60, or 90 days | Not required | Ecommerce, wholesale, B2B marketplaces |

| Hokodo | European B2B ecommerce checkout | 14, 30, 45, 60, 90 days | Not required | Ecommerce, wholesale, distribution |

Most of these providers focus on the seller's side, helping vendors offer terms at their own checkout. That works well if you buy repeatedly from one merchant.

If you want flexible payment terms across every vendor instead of one at a time, a procurement and finance platform may be a better fit. If you're evaluating tools more broadly, our guide to the best procurement software is a good starting point.

B2B BNPL vs. B2C BNPL

Consumer BNPL and business BNPL share a name and a basic idea, but they behave differently once you look at purchase size, approval, and terms.

| Feature | B2B BNPL | B2C BNPL |

| Typical purchase size | Hundreds to hundreds of thousands of dollars | Tens to a few thousand dollars |

| Buyer | A business, often with multiple approvers | An individual consumer |

| Approval | Business credit check and underwriting | Quick personal credit or soft check |

| Repayment terms | Net 30–90 days or scheduled installments | Usually four installments over six weeks |

| Primary goal | Manage cash flow and working capital | Spread out a single discretionary purchase |

B2B BNPL vs. trade credit

BNPL and trade credit both let you pay later, but they place the risk and the work in different hands.

| Feature | B2B BNPL | Trade credit |

| Who extends the payment | A third-party BNPL provider | The seller, directly to the buyer |

| Approval speed | Minutes, through an automated check | Days, after a manual credit application |

| Who carries nonpayment risk | The provider, which pays the seller up front | The seller, who waits to be paid |

| Flexibility | Adjustable terms and installment options | Fixed terms like net 30, 45, or 60 days |

| When the seller gets paid | At the point of sale | At the end of the term |

B2B BNPL market stats

B2B customer demand for flexible payment is reshaping how businesses purchase, and the data shows it:

- The global B2B BNPL market is projected to grow from $247.9 billion in 2026 to $466.6 billion by 2030, a 17.1% compound annual growth rate, according to ResearchAndMarkets.com data.

- That same report found global B2B BNPL payments will become a standard feature embedded across B2B marketplaces and ERP procurement portals by 2028.

- Demand is coming straight from buyers. In a worldwide survey, 85% of B2B buyers said they want to defer payment to suppliers, and nearly 60% preferred trade credit for large purchases.

What the experts say

How does B2B BNPL work?

Approval usually takes only a few minutes. A typical B2B BNPL transaction follows these steps:

- Shop for the goods or services your business needs and add them to your cart.

- Select BNPL at checkout.

- Provide identifying details, such as business name, address, and contact information, for a quick electronic background and credit check that sets your buying limit, repayment terms, and any applicable fees.

- Review and sign the credit agreement outlining the terms and conditions once you're approved.

- Let the seller receive confirmation of the approved transaction along with a remittance schedule.

- Take delivery of your order after the seller fulfills it.

- Make payments on schedule until the balance clears. On-time payments keep your account in good standing and improve your access to credit for future purchases.

Benefits of B2B BNPL for buyers

BNPL gives both sides a fast, secure way to transact, but the buyer-side advantages go further:

- Easier approvals. Traditional credit accounts can take days of paperwork before you get a decision. Because the provider assumes the default risk and guarantees the seller full payment, vendors can approve and fulfill BNPL orders much faster.

- Better cash flow management. Smaller payments spread over time let you keep cash on hand for payroll, inventory, and other priorities. For sectors with uneven revenue, that flexibility matters. See our guide to retail cash flow management for tactics that pair well with BNPL.

- Faster growth. Quick fulfillment helps businesses that don't sit on large cash reserves invest in new products, expand distribution, or ramp up marketing without waiting to save up.

- Fewer invoices to process. Instead of tracking dozens of individual due dates, you make regular payments through one platform, which cuts paperwork and reconciliation time.

- More predictable budgeting. Flexible terms give finance teams a clearer forward view of cash commitments, which makes forecasting and approving future investments easier.

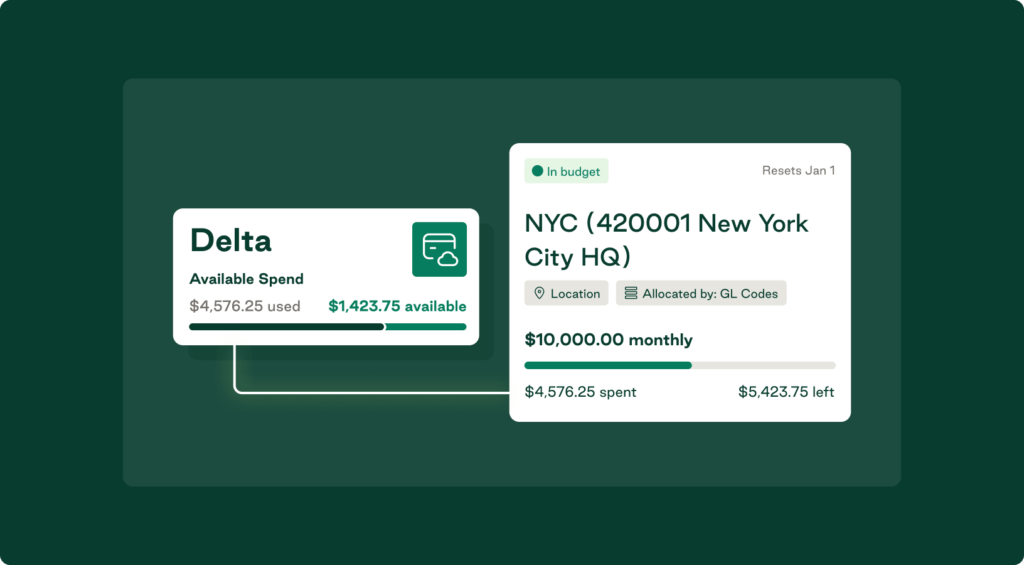

Some buyers get similar flexibility from virtual cards, which add per-purchase spend controls and built-in float without a separate financing application.

B2B BNPL with Order.co Financial Offerings

Unlock capital advances of up to $500k, net terms for all vendors and virtual cards with Order.co, an easy and affordable partner for your business’s growth.

Is B2B BNPL right for your business?

BNPL makes the most sense when you're facing a large or seasonal purchase, your cash flow could use more stability, or you want to avoid the interest and reconciliation that come with corporate cards.

The catch with most BNPL tools is that they work merchant by merchant. You get terms at one vendor's checkout, but not across your whole vendor list, and the financing sits outside your purchasing workflow.

In addition to providing BNPL options, Order.co takes a broader approach. As a procurement and finance automation platform, it combines purchasing, payments, and flexible net terms in one place, so payment flexibility is built into how your team buys.

You can extend net terms across all your vendors, pay through virtual cards, and keep every purchase coded to the right GL line item for a faster close. And control starts at the catalog level, where only pre-approved products and vendors are visible to buyers, so compliant purchasing is the default path.

Pair that with BNPL, spend management software, and AP automation, and you get a single procure-to-pay system instead of a stack of disconnected tools.

To see how you can benefit from flexible terms and automated purchasing working together, schedule a demo of Order.co.

FAQs about B2B BNPL

B2B buy now, pay later is a payment option that lets a business buy goods or services right away and pay for them later, either in installments or on extended net terms. A third-party provider pays the seller up front and collects payment from the buyer over an agreed schedule. It helps procurement and finance teams take delivery without using all their cash at once.

Both let a buyer pay later, but the risk sits in different places. With trade credit, the seller extends terms directly and waits to be paid, carrying the nonpayment risk. With B2B BNPL, a third-party provider pays the seller up front and collects from the buyer, so approval is usually faster.

Established B2B BNPL providers include TreviPay, Resolve, Balance, Mondu, and Hokodo. They differ in the terms they offer, the regions they serve, and whether they focus on enterprise programs or smaller sellers. Order.co takes a broader approach, building flexible net terms and virtual cards into a full procurement and finance platform rather than offering embedded financing at a single vendor's checkout.

Get started

Schedule a demo to see how Order.co can simplify buying for your business.

"*" indicates required fields